Popular Courses

COMM 217

Concordia University

ACCT 2301

The University of Texas at Dallas

Intro to Financial Accounting

General Course

COMM 293

University of British Columbia

Intro to Financial Accounting

University Study Guides

MGCR 211

McGill University

ACCT 1220

University of Guelph

Intro to Financial Accounting

University Study Guides

ACCT 217

University of Calgary

ADMS 2500

York University

COMMERCE 1AA3

McMaster University

ACCTG 211

University of Alberta

ACC 100

Toronto Metropolitan University

COMM 111

Queen's University

ADM 1340

University of Ottawa

BU127

Wilfrid Laurier University

RSM219H1

University of Toronto

ACCT 2301

Houston

ACCT 2301

Houston

COMM 1101

Dalhousie University

0:00 / 0:00

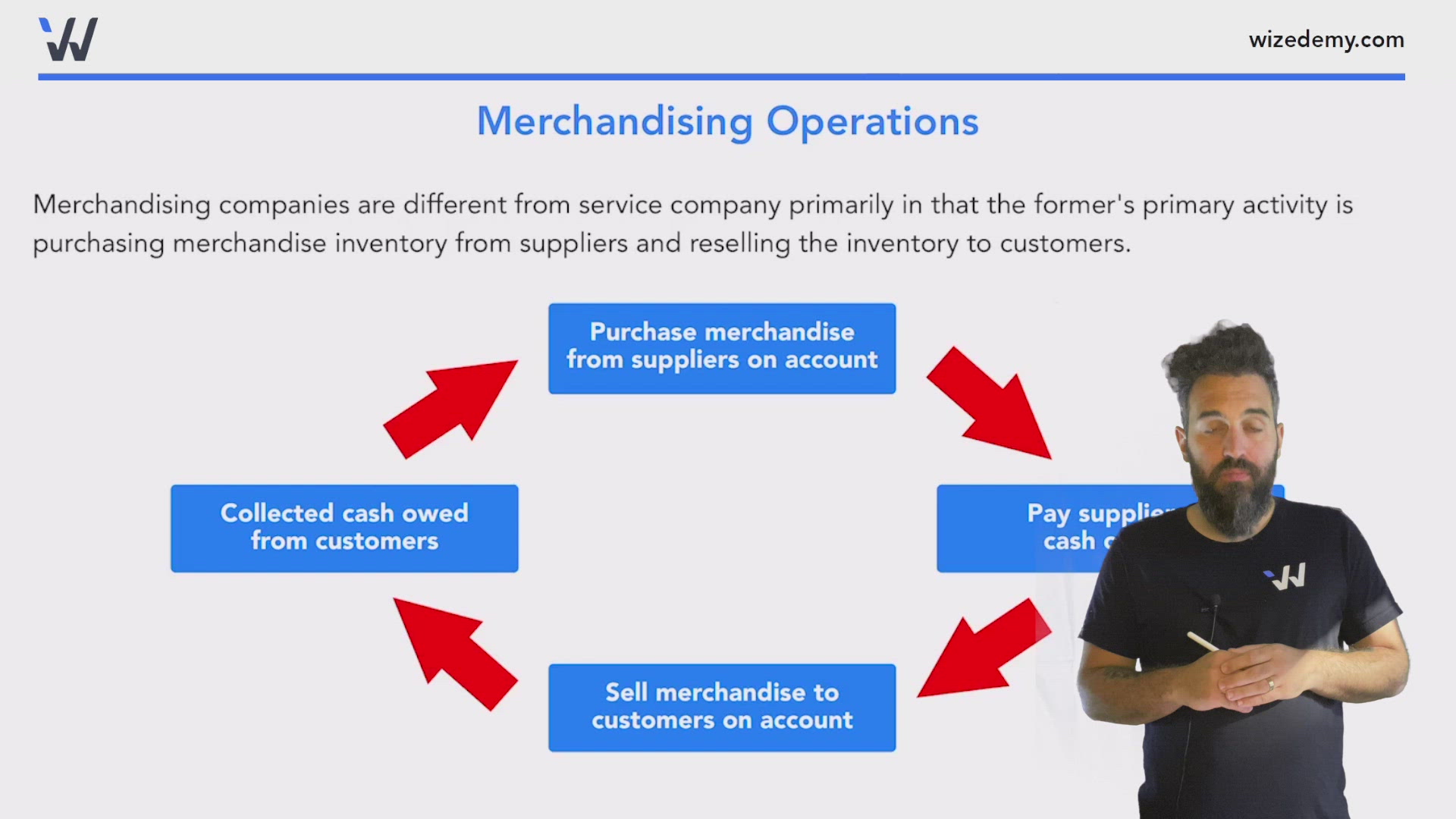

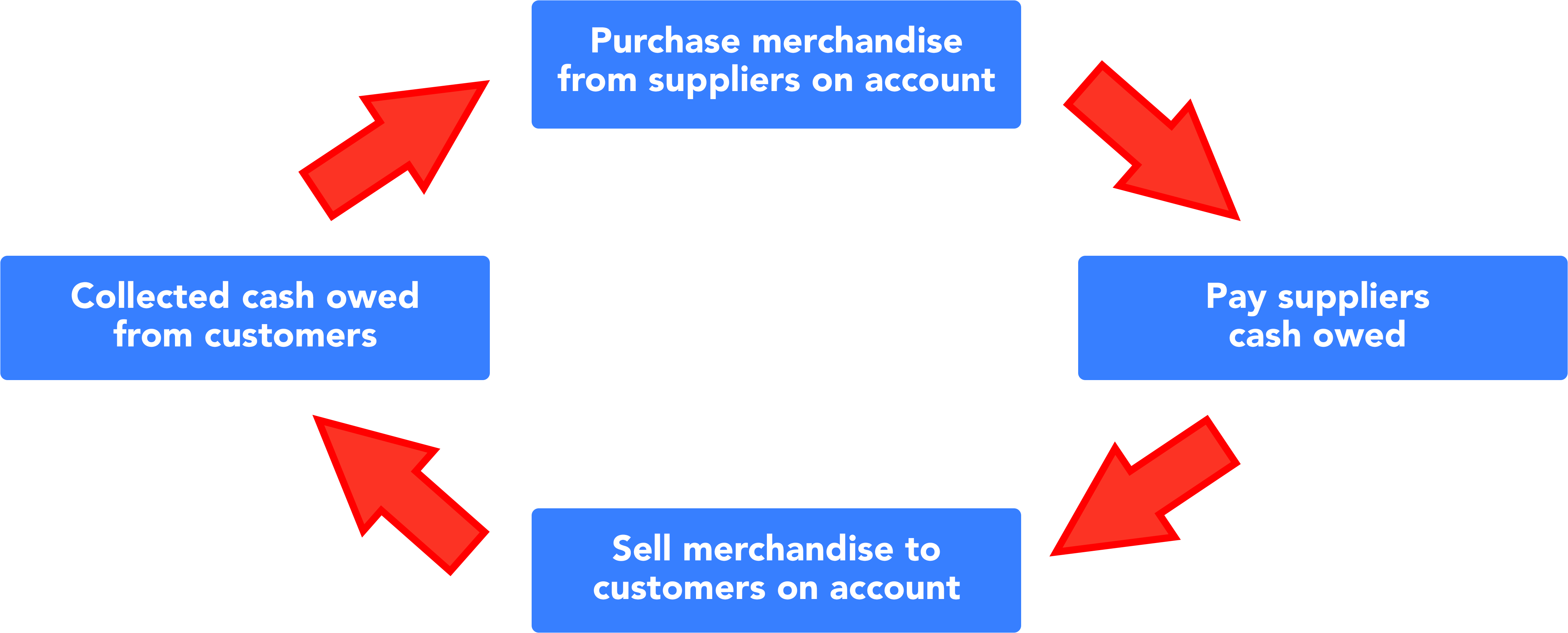

Merchandising Operations

Merchandising companies are different from service company primarily in that the former's primary activity is purchasing merchandise inventory from suppliers and reselling the inventory to customers.

Net Sales

- Sales revenue: Gross amount of sales made before considering returns and discounts.

- Sales discounts: Discounts given to customers for paying their account balance quickly.

- Sales returns and allowances: Customer returns or rebates given to dissatisfied customers.

Revenue Recognition

Revenue is recognized when the following conditions are met:

- The seller has transferred to the buyer the significant risks and rewards of owning the goods

- The seller retains no control over the goods sold

- The amount of revenue earned can be measured reliably.

- It is probable that the economic benefit (payment) will be received by the seller

- The cost incurred or to be incurred can be measured reliably

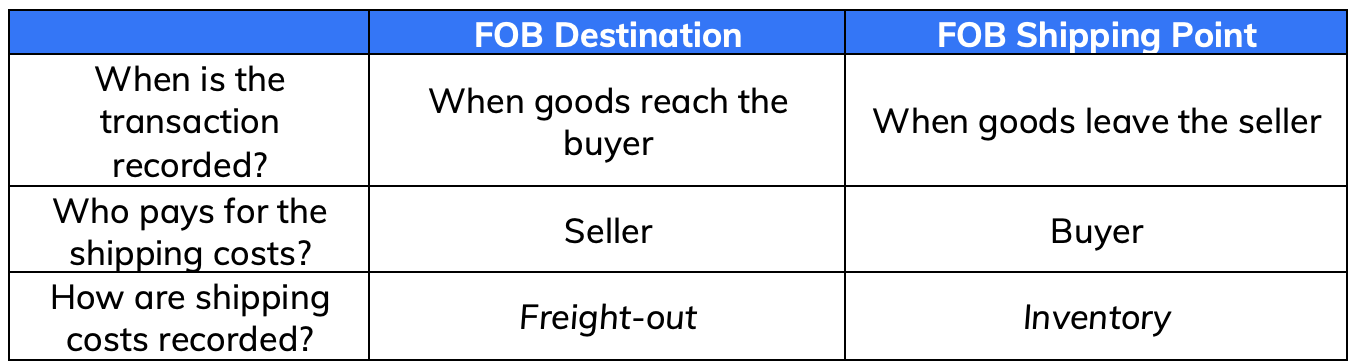

Shipping Terms