Wize University Introduction to Financial Accounting Textbook > Merchandising

Recording Purchases - Perpetual Inventory

Popular Courses

COMM 217

Concordia University

ACCT 2301

The University of Texas at Dallas

Intro to Financial Accounting

General Course

COMM 293

University of British Columbia

Intro to Financial Accounting

University Study Guides

MGCR 211

McGill University

ACCT 1220

University of Guelph

Intro to Financial Accounting

University Study Guides

ACCT 217

University of Calgary

ADMS 2500

York University

COMMERCE 1AA3

McMaster University

ACCTG 211

University of Alberta

ACC 100

Toronto Metropolitan University

COMM 111

Queen's University

ADM 1340

University of Ottawa

BU127

Wilfrid Laurier University

RSM219H1

University of Toronto

ACCT 2301

Houston

ACCT 2301

Houston

COMM 1101

Dalhousie University

0:00 / 0:00

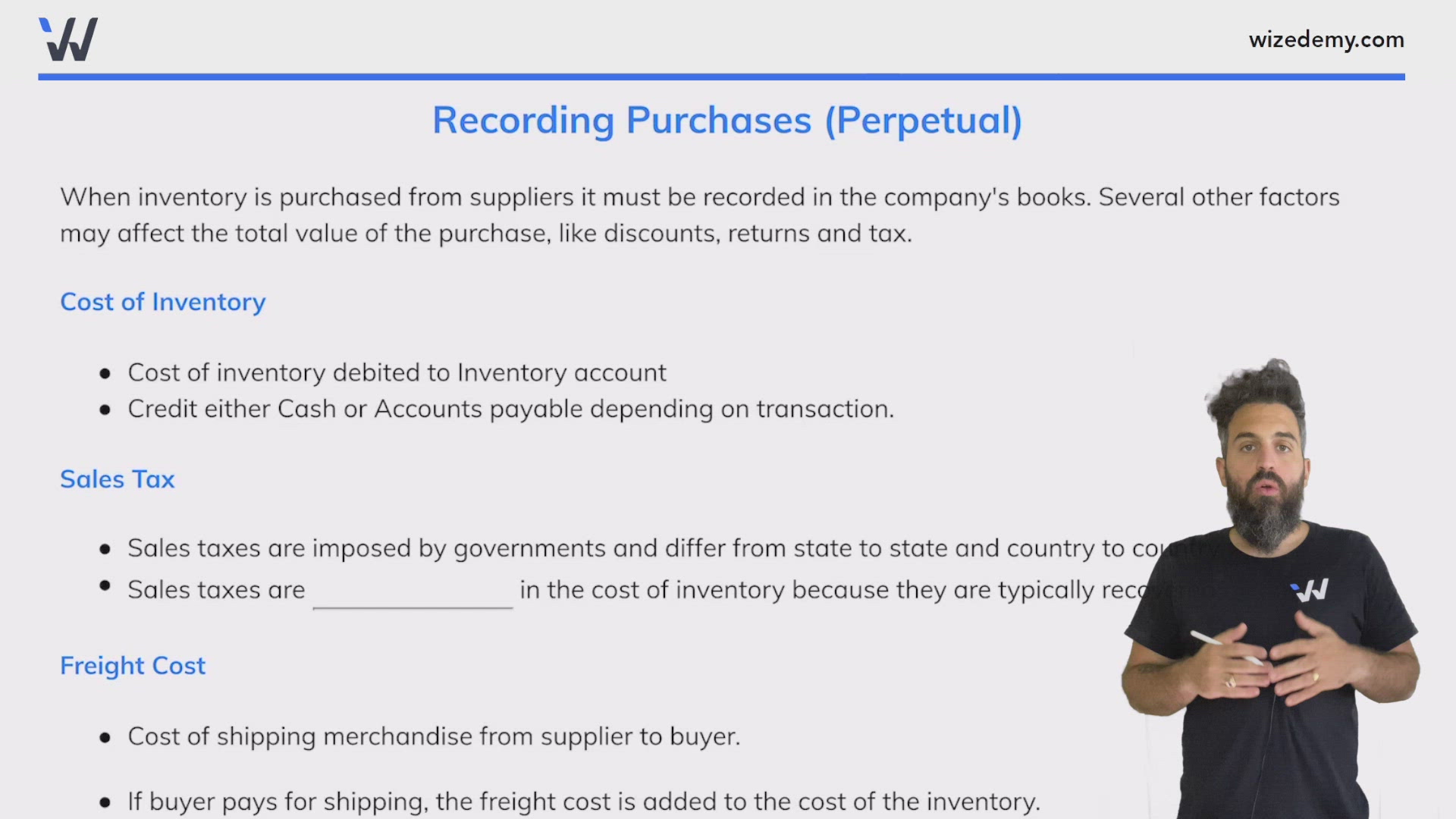

Recording Purchases (Perpetual)

When inventory is purchased from suppliers it must be recorded in the company's books. Several other factors may affect the total value of the purchase, like discounts, returns and tax.

Cost of Inventory

- Cost of inventory debited to Inventory account

- Credit either Cash or Accounts payable depending on transaction.

Sales Tax

- Sales taxes are imposed by governments and differ from state to state and country to country.

- Sales taxes arenot includedin the cost of inventory because they are typically recovered by the buyer.

Freight Cost

- Cost of shipping merchandise from supplier to buyer.

- If buyer pays for shipping, the freight cost is added to the cost of the inventory.

- Who pays for shipping?

- FOB destination: seller is responsible for the goods until they reach the destination.

- Thesellerpays for the shipping.

- Sale is recorded the day the goods reach the destination.

- Shipping cost not recorded by the buyer.

- FOB shipping point: buyer is responsible for the goods as soon as they are shipped.

- Thebuyerpays for the shipping.

- Sale is recorded the day the goods are shipped.

- Shipping cost added to cost of inventory by the buyer.

0:00 / 0:00

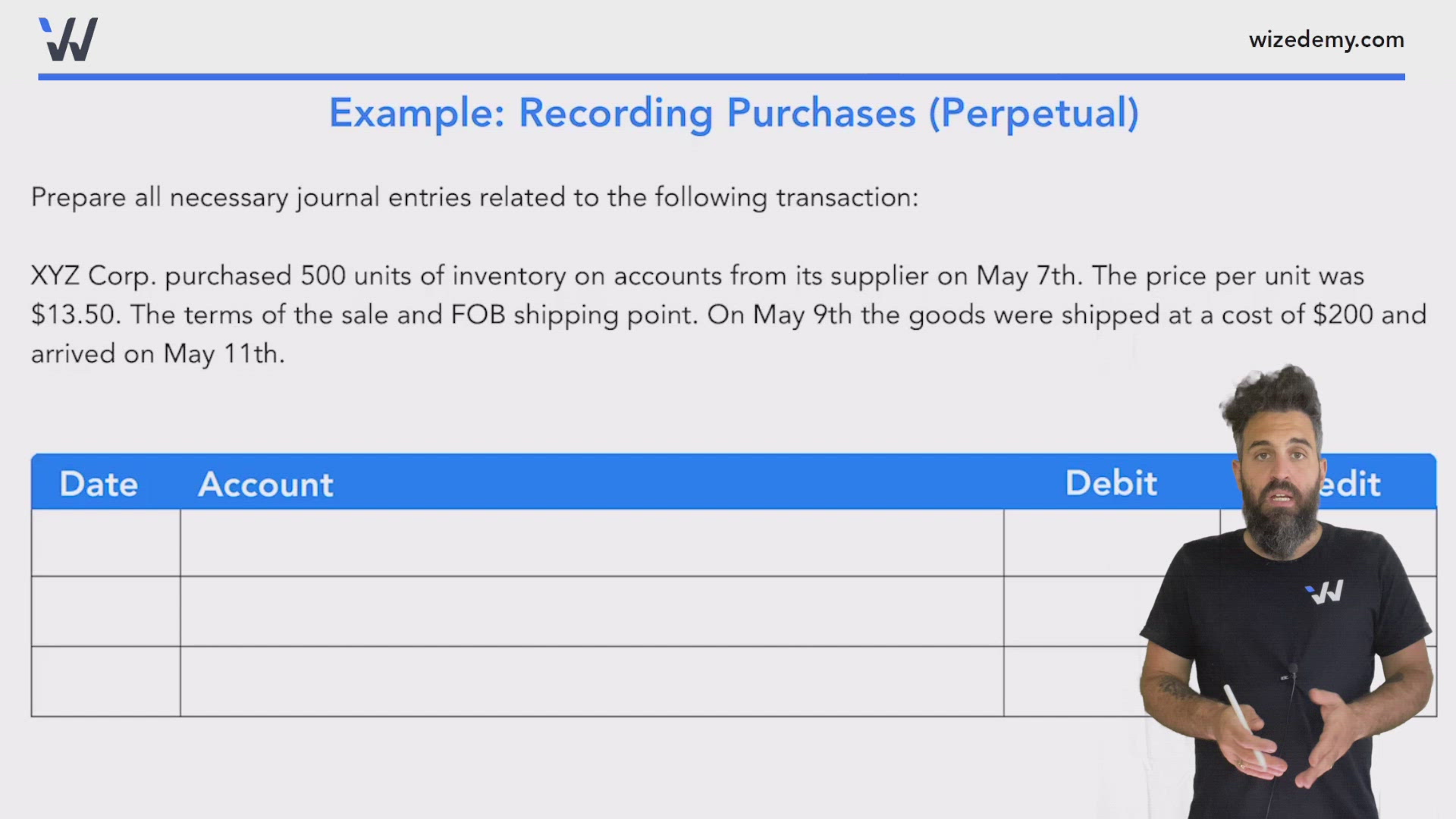

Example: Recording Purchases (Perpetual)

Prepare all necessary journal entries related to the following transaction:

XYZ Corp. purchased 500 units of inventory on accounts from its supplier on May 7th. The price per unit was $13.50. The terms of the sale and FOB shipping point. On May 9th the goods were shipped at a cost of $200 and arrived on May 11th.

Practice: Recording Purchases (Perpetual)

ABC Inc. is a furniture retailer in Seattle, management needs your help to prepare its journal entries for the year before preparing its financial statements. The following events took place during January 2020. The company uses the perpetual inventory system.

Jan 1: Began the year with $60,000 in inventory.

Jan 7: Purchased 100 units for $120 each from Supplier A on account. The terms were 2/10, n/45 and FOB shipping point.

Jan 9: Supplier A shipped the goods, the cost of the shipping was $500.

Jan 10: Received the goods from Supplier A.

Jan 13: Returned 5 defective units to Supplier A.

Jan 17: Paid entire balance to Supplier A.

Jan 18: Purchased 200 units for $90 each from Supplier B on account. The terms were 1/5, n/60 and FOB destination.

Jan 20: Supplier B shipped the goods, the cost of the shipping was $300.

Jan 22: Received the goods from Supplier B.

Jan 30: Paid balance in full to Supplier B.

Jan 31: Returned 1 defective unit to Supplier A.

Prepare the journal entry to record the transaction on January 18th.

Transactions:

| Account | Debit | Credit |

|---|---|---|