Popular Courses

COMM 217

Concordia University

COMM 217

Concordia University

ACCT 2301

The University of Texas at Dallas

Intro to Financial Accounting

General Course

COMM 293

University of British Columbia

Intro to Financial Accounting

University Study Guides

MGCR 211

McGill University

ACCT 1220

University of Guelph

Intro to Financial Accounting

University Study Guides

ACCT 217

University of Calgary

ADMS 2500

York University

COMMERCE 1AA3

McMaster University

ACCTG 211

University of Alberta

BU127

Wilfrid Laurier University

RSM219H1

University of Toronto

COMM 1101

Dalhousie University

ACCT 2301

Houston

ACCT 2301

Houston

AFM 101

University of Waterloo

ACTG 2010

York University

0:00 / 0:00

Bank Reconciliation

At the end of each month, companies must reconcile their bank statement balance with the cash balance in the general ledger to determine the correct amount of cash that should be reported. This is necessary because certain items appear on the bank statement but not in the ledger, and others appear in the ledger but not on the bank statement.

Bank Statement Balance

- Cash balance according to bank's records

- Sent periodically to the company

- Only reflects transactions that have been recorded by the bank

Book Balance

- Cash balance according to company's bookkeeping

- Only reflects transactions that have been recorded in the company's general ledger

Wize Tip

Both the bank statement balance and book balance are incorrect until they are adjusted during the bank reconciliation process.

Deposits in Transit

- Also called outstanding deposits

- Cash or cheques received but not yet deposited

- Cash of cheques deposited after statement is printed

- Increases bank statement balance

Outstanding Cheques

- Cheques written but not yet taken from bank account

- Decreases bank statement balance

Bank Errors

- Over or understatement of deposits or withdrawals

- Could increase or decrease bank statement balance depending on error

- Example: Bank incorrectly debited a $400 cheque as $4,000.

Deposits by Bank

- Any deposit of cash into account by the bank

- Increases book balance

- Example: wire transfers, collections of notes by the bank, interest on account balance

Bank Service Charges

- Expense charged by the bank for services

- Decreases book balance

Non-Sufficient Funds Check (NSF)

- Check deposited and rejected by the bank

- Check issuer did not have enough money in their account

- Decreases book balance

Book Errors

- Bookkeeping errors affecting cash

- Could increase or decrease book balance depending on error.

- Example: Incorrectly recording a cash sale as $750 instead of $570.

Bank Reconciliation Statement

Bank Reconciliation Journal Entries

- Record only adjustments to book balance

- Should always contain cash account.

- Each adjustment affects another financial statement account.

0:00 / 0:00

Example: Bank Reconciliation

ABC Inc. just received its June 30th bank statement. According to the bank statement the company has $24,205.88 in cash but according to the company's ledger the cash balance is $26,326.60.

The following information is available:

- Cheque number 345 for $1,540.43 is still outstanding.

- Cheque number 341 was incorrectly debited from the account as $704.40 instead of $658.85.

- Bank memo states that a wire transfer of $1,000 was received from a customer who was paying off a previous purchase.

- Earned interest of $100 on account balance.

- Received a cheque from a customer for $745.60 but the cheque has not yet been deposited.

- Customer's cheque for $350 returned as NSF, bank charged ABC Inc. $20 service fee.

- Bookkeeper incorrectly recorded a cash purchase of inventory as $400 instead of $4,000.

Prepare the bank reconciliation statement and adjusting journal entries on June 30th.

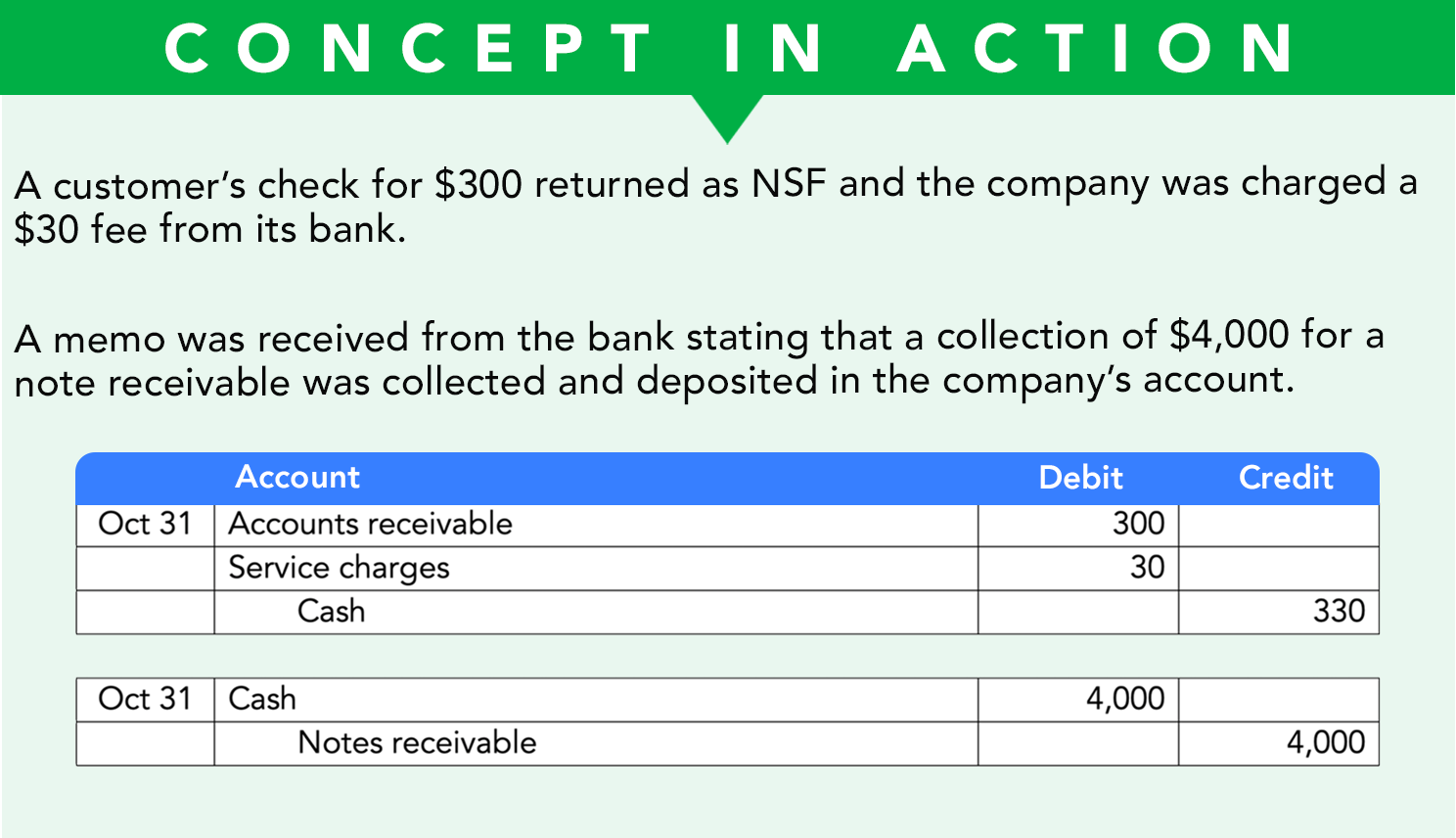

Practice: Bank Reconciliation

KG Corp.'s October 31st, 2020 bank statement balance is $35,639.44 and its book balance is $28,010.45. Using the following information, perform a bank reconciliation.

- Cheque number 752 and 756 are still outstanding. Cheque 752 was written for $2,400.55 and cheque 756 was written for $3,213.44.

- A bank memo states that a long-term note of $5,500 note receivable was collected by the bank, this includes $500 of interest on the note.

- Incorrectly recorded the purchase of $450 of inventory as $540.

- A customer's check of $500 returned NSF.

- Monthly bank service charges totalled $75.

- A deposit of $3,000 in cash made on October 31st does not appear on the bank statement yet.

What is the correct adjusted cash balance at the end of October 2020?