Wize University Introduction to Financial Accounting Textbook > Investments

Fair Value Through Profit or Loss

Popular Courses

ACCT 2301

The University of Texas at Dallas

Intro to Financial Accounting

General Course

COMM 293

University of British Columbia

Intro to Financial Accounting

University Study Guides

Intro to Financial Accounting

University Study Guides

ACCTG 211

University of Alberta

ACCT 2301

Houston

ACCT 2301

Houston

AFM 101

University of Waterloo

BUSINESS 3321K

Western University

ACCT-1510

University of Windsor

ADMN 1221H

Trent University

ACC 110

Toronto Metropolitan University

ACC 1100

University of Manitoba

ACCT 1201

Northeastern University

ACC 221

Miami University - Ohio

ACTG 2011

York University

ACTG 1P01

Brock University

ACCT 2101

University of Georgia

ACCT 207

University of Delaware

0:00 / 0:00

Fair Value Through Profit or Loss

This method of accounting for non-strategic investments requires periodic adjustments in the value of the investment to reflect the fair value (market value). This method is commonly used for investments that are marked for trading.

Trading Investments

- Investments held for a short-period of time

- Intention is to trade the investments frequently

Recording the Acquisition

- Recorded as Trading Investments

- Includes all costs related to acquisition

- Example: Price of shares, brokerage fees, commissions

Recording Dividends

- Recorded as revenue

- No adjustments are needed for timing because dividends do not accrue like interest.

Recording Adjustment to Fair Value

- Value of asset adjusted to fair value

- Record change as unrealized gain or loss

Recording Sale

- Record net proceeds from sale

- Sale price less any selling expenses like brokerage fees and commissions

- Recognize realized gain or loss

- Difference between proceeds from sale and carrying value

0:00 / 0:00

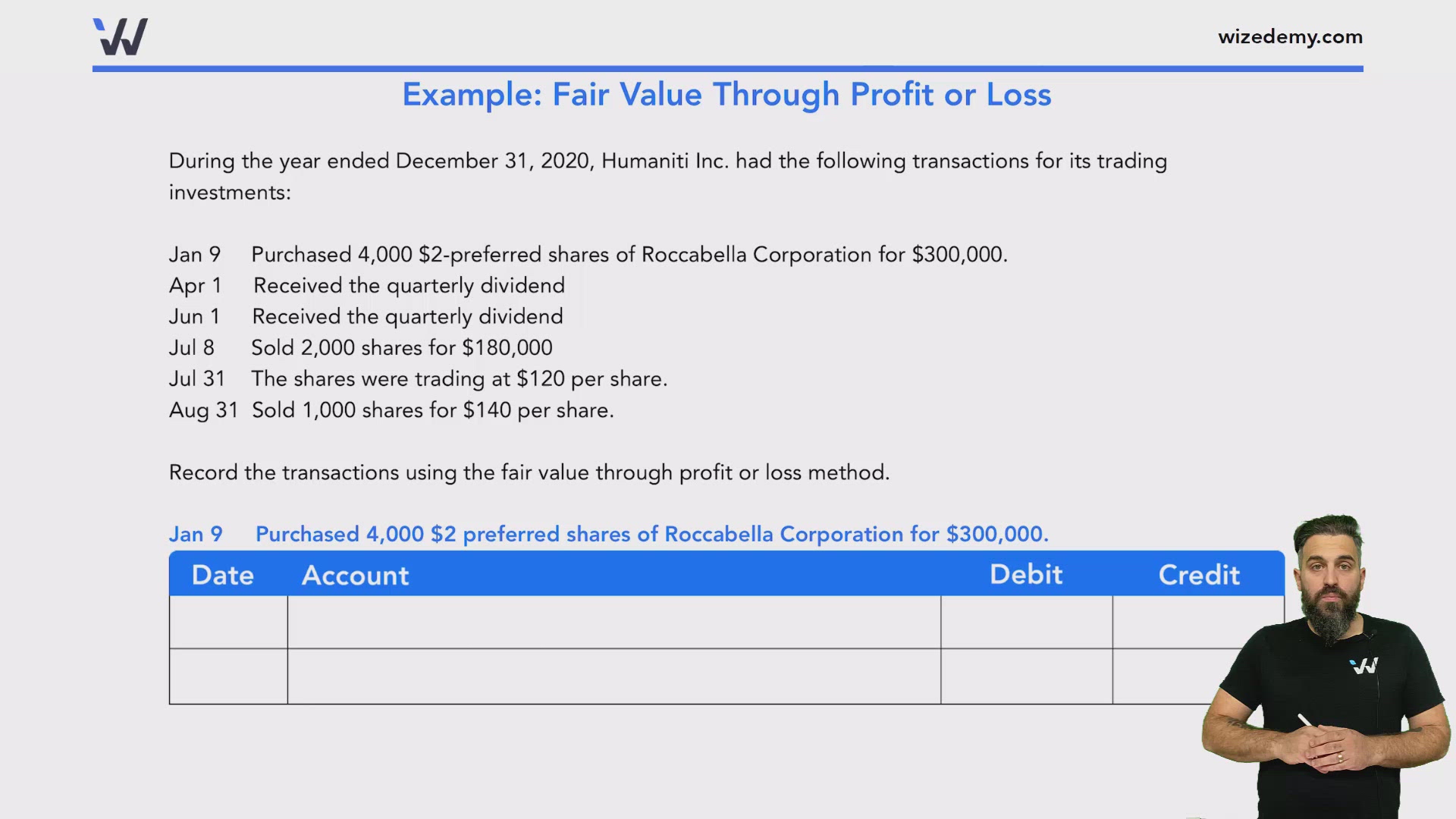

Example: Fair Value Through Profit or Loss

During the year ended December 31, 2020, Humaniti Inc. had the following transactions for its trading investments:

Jan 9 Purchased 4,000 $2-preferred shares of Roccabella Corporation for $300,000.

Apr 1 Received the quarterly dividend

Jun 1 Received the quarterly dividend

Jul 8 Sold 2,000 shares for $180,000

Jul 31 The shares were trading at $120 per share.

Aug 31 Sold 1,000 shares for $140 per share.

Record the transactions using the fair value through profit or loss method.

Jan 9 Purchased 4,000 $2 preferred shares of Roccabella Corporation for $300,000.

Apr 1 Received the quarterly dividend

Jun 1 Received the quarterly dividend

Jul 8 Sold 2,000 shares for $180,000

Jul 31 The shares were trading at $120 per share.

Aug 31 Sold 1,000 shares for $140 per share.

0:00 / 0:00

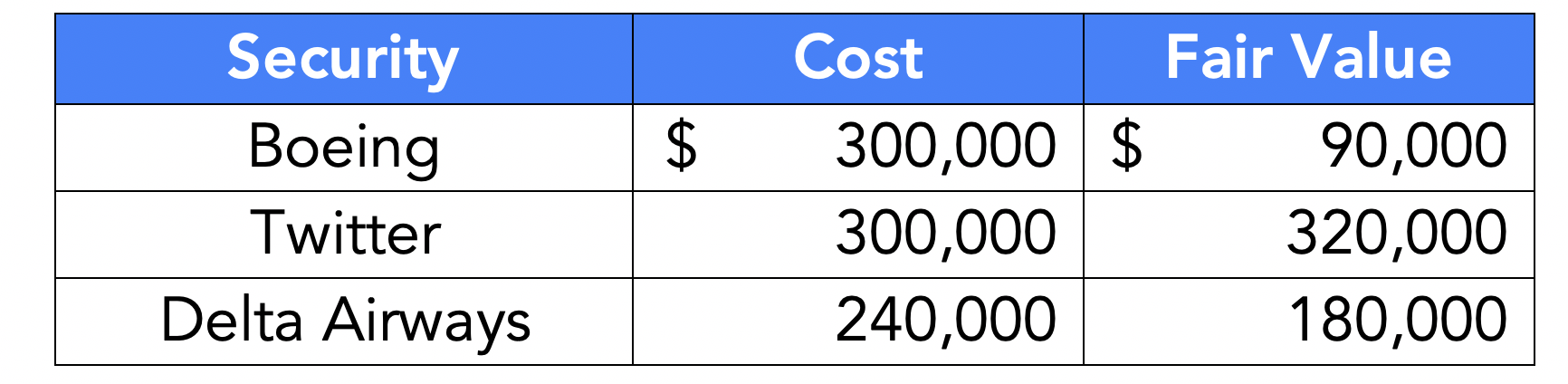

Example: Fair Value Through Profit and Loss

Karla Inc. had the following three securities in its trading portfolio on December 31st, 2019:

Prepare the adjusting entry at December 31st, 2019 to report the portfolio at its fair value.

Practice: Fair Value Through Profit or Loss

On February 17th Apple Inc. purchased 5,000 common shares of Microsoft Corp. for $1,000,000, these shares were marked for trading. On April 12th, Apple received a $40,000 cash dividend from Microsoft. On June 30th, Microsoft was trading at $280 per share and on August 19th, Apple Inc. sold 3,000 shares of Microsoft for $816,000.

Prepare the journal entries to record

The purchase of shares on February 17th

Transactions:

| Account | Debit | Credit |

|---|---|---|

Practice: Fair Value Through Profit or Loss

XYZ Inc. had the following three securities in its trading portfolio on December 31st, 2021:

Prepare the adjusting entry at December 31st, 2021 to report the portfolio at its fair value.

Transactions:

| Account | Debit | Credit |

|---|---|---|