Popular Courses

COMM 217

Concordia University

Intro to Financial Accounting

General Course

ACCT 2301

The University of Texas at Dallas

COMM 293

University of British Columbia

Intro to Financial Accounting

University Study Guides

MGCR 211

McGill University

ACCT 1220

University of Guelph

Intro to Financial Accounting

University Study Guides

ACCT 217

University of Calgary

ADMS 2500

York University

COMMERCE 1AA3

McMaster University

ACCTG 211

University of Alberta

COMM 111

Queen's University

ADM 1340

University of Ottawa

BU127

Wilfrid Laurier University

ACCT 2301

Houston

ACCT 2301

Houston

RSM219H1

University of Toronto

COMM 1101

Dalhousie University

AFM 101

University of Waterloo

0:00 / 0:00

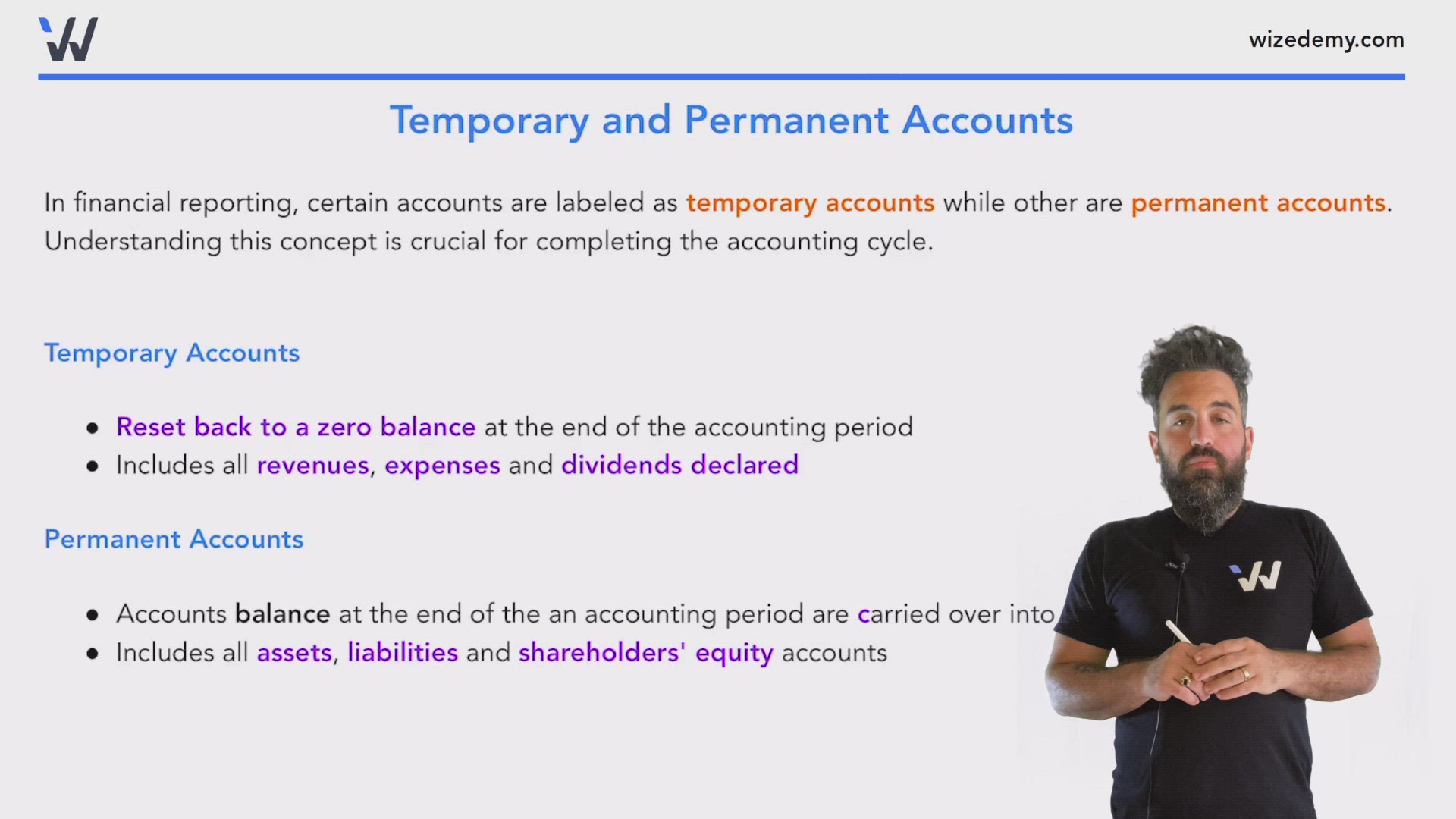

Temporary and Permanent Accounts

In financial reporting, certain accounts are labeled as temporary accounts while other are permanent accounts. Understanding this concept is crucial for completing the accounting cycle.

Temporary Accounts

- Reset back to a zero balance at the end of the accounting period

- Includes all revenues, expenses and dividends declared

Permanent Accounts

- Accounts balance at the end of the an accounting period are carried over into the following period

- Includes all assets, liabilities and shareholders' equity accounts

0:00 / 0:00

Closing Entries

Temporary accounts must be reset (closed) at the end of the accounting period, this is done by writing closing entries.

Four Closing Entries

- Close revenues and contra-revenues to Income Summary

- Close expenses to Income Summary

- Close Income Summary to Retained Earnings

- Close Dividends Declared to Retained Earnings

0:00 / 0:00

Post-Closing Trial Balance

The final step in the accounting cycle is preparing the post-closing trial balance which lists the account balances that will be carried over into the next period.

What it looks like

0:00 / 0:00

Example: Closing Entries

Prepare the closing entries using the following income statement.

Journal entry to close revenues

Journal entry to close expenses

Journal entry to transfer income summary to retained earnings

Journal entry to close dividends declared

Practice: Closing Entries

Prepare the closing entries for Wizedemy for the year ended December 31st, 2020. During the year, the company declared $20,000 of dividends.

Journal entry to close revenues

Transactions:

| Account | Debit | Credit |

|---|---|---|