Popular Courses

COMM 217

Concordia University

ACCT 2301

The University of Texas at Dallas

Intro to Financial Accounting

General Course

COMM 293

University of British Columbia

Intro to Financial Accounting

University Study Guides

MGCR 211

McGill University

ACCT 1220

University of Guelph

Intro to Financial Accounting

University Study Guides

ACCT 217

University of Calgary

ADMS 2500

York University

COMMERCE 1AA3

McMaster University

ACCTG 211

University of Alberta

COMM 111

Queen's University

ADM 1340

University of Ottawa

BU127

Wilfrid Laurier University

RSM219H1

University of Toronto

COMM 1101

Dalhousie University

ACCT 2301

Houston

ACCT 2301

Houston

AFM 101

University of Waterloo

0:00 / 0:00

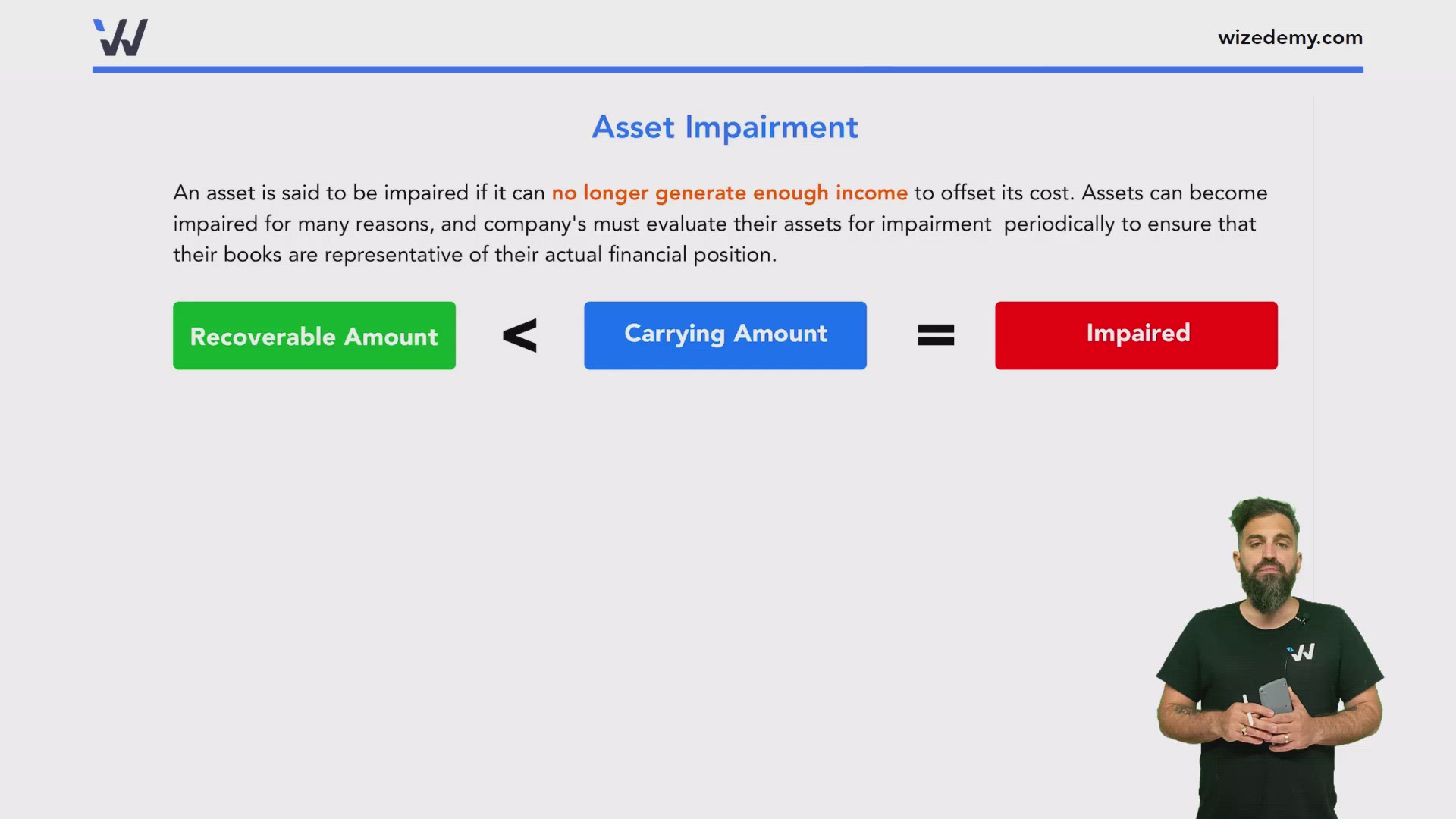

Asset Impairment

An asset is said to be impaired if it can no longer generate enough income to offset its cost. Assets can become impaired for many reasons, and company's must evaluate their assets for impairment periodically to ensure that their books are representative of their actual financial position.

Recoverable Amount

- The total amount of income that the asset will generate over its remaining life.

- Value in use: The amount of income generated through the use of the asset.

- Fair value: The amount of income generated if the asset is sold less any costs to sell.

Recording Impairment

- Asset's value must be decreased to recoverable amount

- Debit Impairment loss

- Credit Asset

0:00 / 0:00

Example: Asset Impairment

A review of ABC Inc. long-term assets on December 31st, 2027 determined the following information:

Prepare the journal entry to record the impairment loss.

Practice: Asset Impairment

A local UPS store in Newport, California uses three trucks to deliver packages. Recently, its newest truck was involved in an accident, the truck was repaired and put back into use. An analysis of the company's fixed assets at the end of the year was conducted to determine this year's impairment loss. The following information is available:

Prepare the journal entry to record the impairment loss.

Transactions:

| Account | Debit | Credit |

|---|---|---|