Wize University Managerial Accounting Textbook > Incremental Analysis

Sell or Process Further

Popular Courses

COMM 305

Concordia University

Managerial Accounting

University Study Guides

Managerial Accounting

University Study Guides

ACC 406

Toronto Metropolitan University

ACCTG 322

University of Alberta

ACCT 2230

University of Guelph

ADM 2341

University of Ottawa

COMMERCE 2AB3

McMaster University

ACTG 2020

York University

COMM 1102

Dalhousie University

ACC 312

The University of Texas at Austin

ACC 242

Arizona State University - Tempe

ACC 202

Michigan State University

ACIS 2116

Virginia Tech

ACG 2071

University of Central Florida

BUS1 21

San José State University

BUS-A 306

Indiana University - Bloomington

ACCT 2102

Temple University

ACCTG-202

San Diego State University

MGMT 20100

Purdue University

0:00 / 0:00

Sell or Process Further

Sometimes a product can be sold at one point in the production process, but can also be processed further into another product, which can then be sold for a higher price.

Things to consider:

- Incremental Revenue and Incremental Cost

- Is the increase in selling price higher than the cost to process further

- If yes, then it should be processed further

- If not, then it should not be processed further

- Joint Costs

- Any single cost that is incurred in order to produce multiple units

- Joint costs are sunk (irrelevant)

Joint Processes

A joint process is an activity that produces more than one product at the same time. Until the split off point all these products are combined and only after the split off point can they be distinguished. The costs of the process are called joint costs and are irrelevant to further decisions.

0:00 / 0:00

Example: Sell-or-Process Further

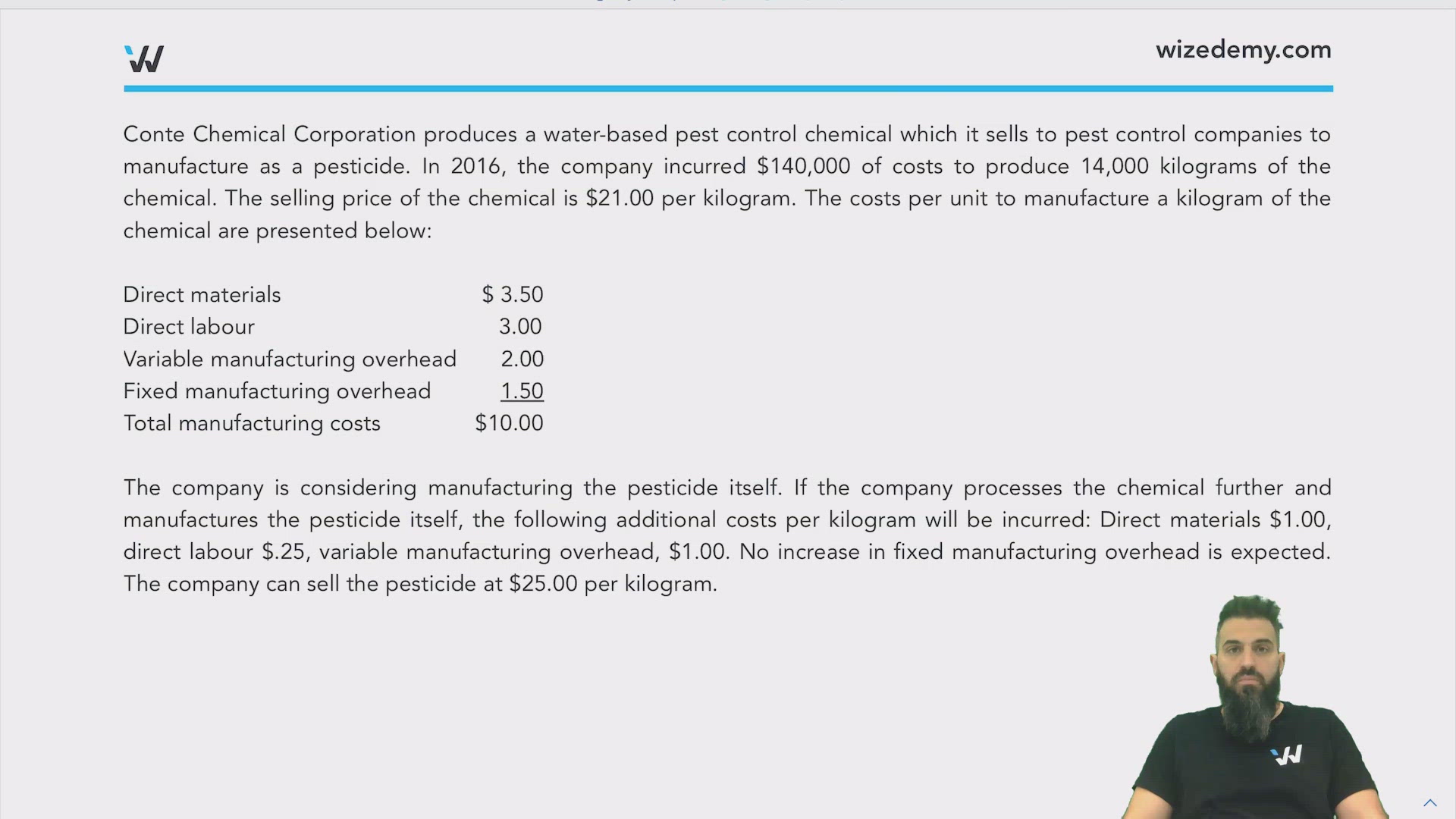

Conte Chemical Corporation produces a water-based pest control chemical which it sells to pest control companies to manufacture as a pesticide. In 2016, the company incurred $140,000 of costs to produce 14,000 kilograms of the chemical. The selling price of the chemical is $21.00 per kilogram. The costs per unit to manufacture a kilogram of the chemical are presented below:

Direct materials $ 3.50

Direct labour 3.00

Variable manufacturing overhead 2.00

Fixed manufacturing overhead 1.50

Total manufacturing costs $10.00

The company is considering manufacturing the pesticide itself. If the company processes the chemical further and manufactures the pesticide itself, the following additional costs per kilogram will be incurred: Direct materials $1.00, direct labour $.25, variable manufacturing overhead, $1.00. No increase in fixed manufacturing overhead is expected. The company can sell the pesticide at $25.00 per kilogram.

Practice: Sell-or-Process Further

A company manufactures three products using the same production process. The costs incurred up to the split-off point are $120,000. These costs are allocated to the products on the basis of their sales value at the split-off point. The number of units produced, the selling prices per unit of the three products at the split-off point and after further processing, and the additional processing costs are as follows.

Which product(s) should be processed further?