Wize University Managerial Accounting Textbook > Standard Costing & Variance Analysis

Variable Overhead Variances

Popular Courses

COMM 305

Concordia University

Managerial Accounting

University Study Guides

Managerial Accounting

University Study Guides

ACC 406

Toronto Metropolitan University

ACCT 2230

University of Guelph

ADM 2341

University of Ottawa

RSM222H1

University of Toronto

COMMERCE 2AB3

McMaster University

ACTG 2020

York University

COMM 1102

Dalhousie University

ACC 312

The University of Texas at Austin

ACC 242

Arizona State University - Tempe

ACC 202

Michigan State University

ACIS 2116

Virginia Tech

ACG 2071

University of Central Florida

BUS1 21

San José State University

BUS-A 306

Indiana University - Bloomington

ACCT 2102

Temple University

ACCTG-202

San Diego State University

MGMT 20100

Purdue University

0:00 / 0:00

Variable Overhead Variances

Variable overhead variances occur when the amount spent on variable manufacturing overhead differs from what was expected according to the standards.

- Spending Variance: Difference between what the variable manufacturing overhead actually cost and what it should have cost given the level of activity during the period.

- The standard price is the predetermined overhead rate

- Efficiency Variance: Difference between the actual hours worked and the hours expected according to the standard. The variance is expressed in dollars using the standard price.

- Total Variance: Sum of the spending and efficiency variance.

What causes a Variable Overhead spending variance?

- Economies of scale (Favourable)

- A decrease in the general prices of indirect supplies and materials. (Favourable)

- More efficient control of cost (Favourable)

- Buying higher quality indirect materials. (Unfavourable)

- A rise in the national minimum wage leading to higher cost of indirect labour. (Unfavourable)

- Inefficient cost control. (Unfavourable)

- Planning errors. (Unfavourable)

What causes a Variable Overhead efficiency variance?

- Using higher quality materials (Favourable)

- Hiring more highly skilled workers (Favourable)

- Using more efficient manufacturing equipment (Favourable)

- Use of cheaper, lower quality materials (Unfavourable)

- Hiring lower skilled workers (Unfavourable)

- Decline in the productivity of manufacturing equipment, wear and tear (Unfavourable)

0:00 / 0:00

Example: Variable Overhead Variances

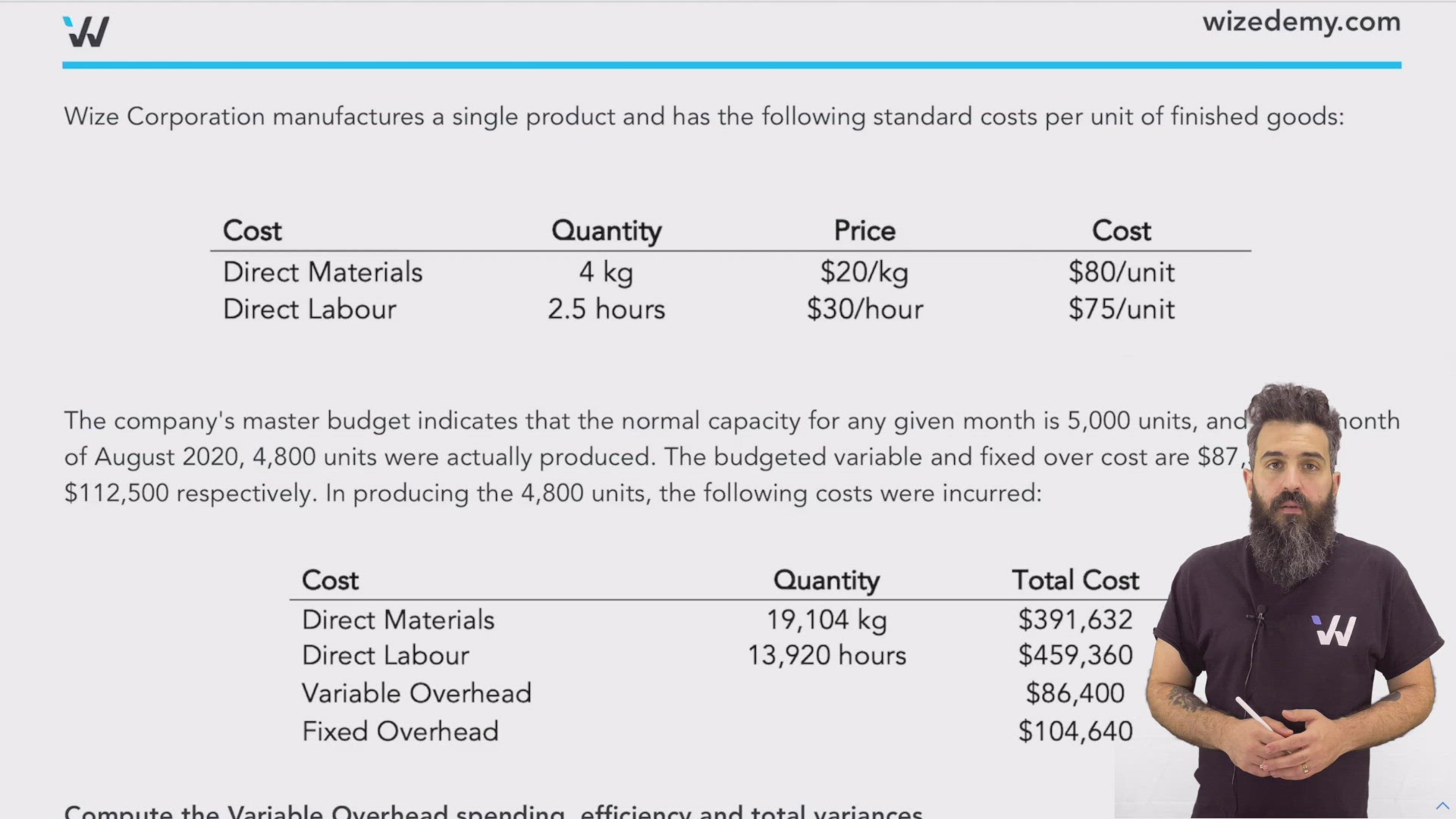

Wize Corporation manufactures a single product and has the following standard costs per unit of finished goods:

The company's master budget indicates that the normal capacity for any given month is 5,000 units, and in the month of August 2020, 4,800 units were actually produced. The budgeted variable and fixed overhead cost are $87,500 and $112,500 respectively. In producing the 4,800 units, the following costs were incurred:

Compute the Variable Overhead spending, efficiency and total variances.

Practice: Variable Overhead Variances

Buono Corporation manufactures fire extinguishers for residual and commercial use. The standard material cost of producing one unit is $30 (3 lbs of material @ $10/lb). The standard labor rate of workers at the company is $15 per hour, and it is expected that each unit will require 1 hour of labor to be produced.

The budgeted overhead cost is $500,000, of which 30% is variable and the rest is fixed. The company's budget is based on producing 10,000 units this year.

At the end of the year, the company had produced 9,300 units and the following costs were incurred:

- Direct materials (31,000 lbs) $308,450

- Direct labor (9,100 hours) $141,050

- Variable overhead: $180,000

- Fixed overhead: $334,550

Answer the following questions, do not use any symbols ($, %, !);

Use the first blank for the value and in the second blank enter F for favorable and U for unfavorable.

Variable overhead spending variance

Variable overhead efficiency variance

Total variable overhead budget variance