Popular Courses

COMM 305

Concordia University

Managerial Accounting

University Study Guides

Managerial Accounting

University Study Guides

ACC 406

Toronto Metropolitan University

ACCT 2230

University of Guelph

ADM 2341

University of Ottawa

RSM222H1

University of Toronto

COMMERCE 2AB3

McMaster University

ACTG 2020

York University

COMM 1102

Dalhousie University

ACC 312

The University of Texas at Austin

ACC 242

Arizona State University - Tempe

ACC 202

Michigan State University

ACIS 2116

Virginia Tech

ACG 2071

University of Central Florida

BUS1 21

San José State University

BUS-A 306

Indiana University - Bloomington

ACCT 2102

Temple University

ACCTG-202

San Diego State University

MGMT 20100

Purdue University

0:00 / 0:00

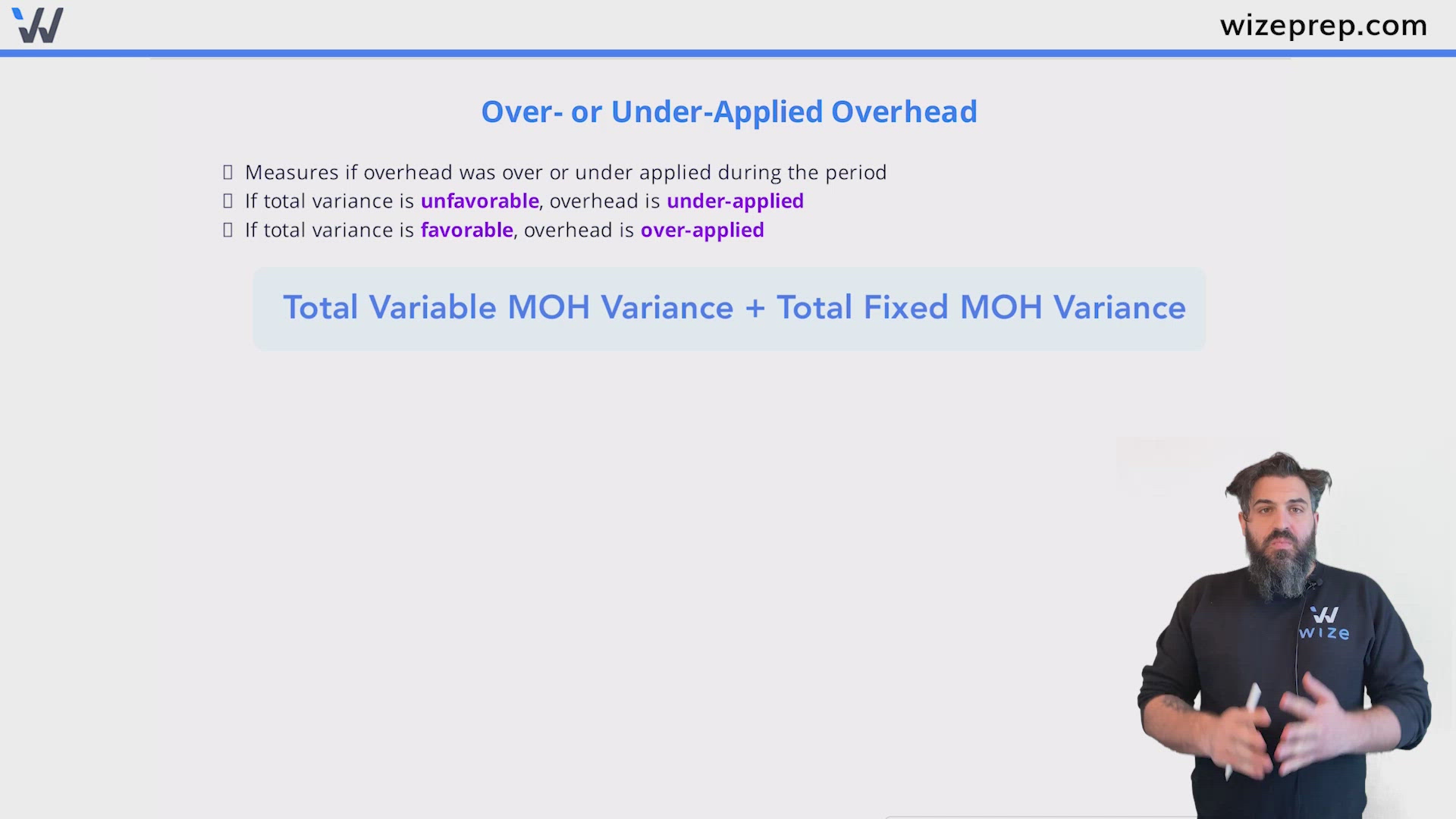

Over- or Under-Applied Overhead

- Measures if overhead was over or under applied during the period

- If total variance is unfavorable, overhead is under-applied

- If total variance is favorable, overhead is over-applied

0:00 / 0:00

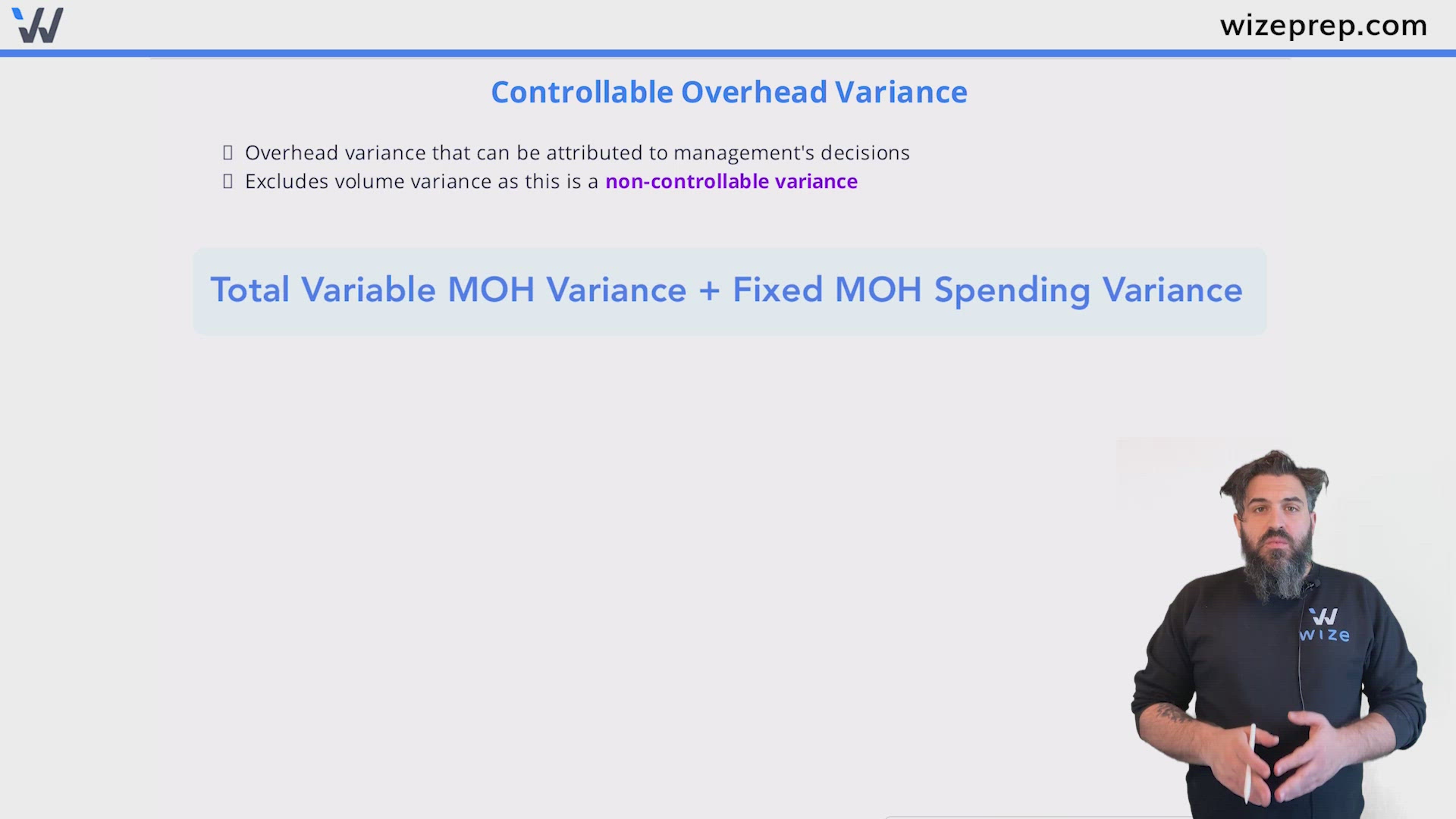

Controllable Overhead Variance

- Overhead variance that can be attributed to management's decisions

- Excludes volume variance as this is a non-controllable variance

0:00 / 0:00

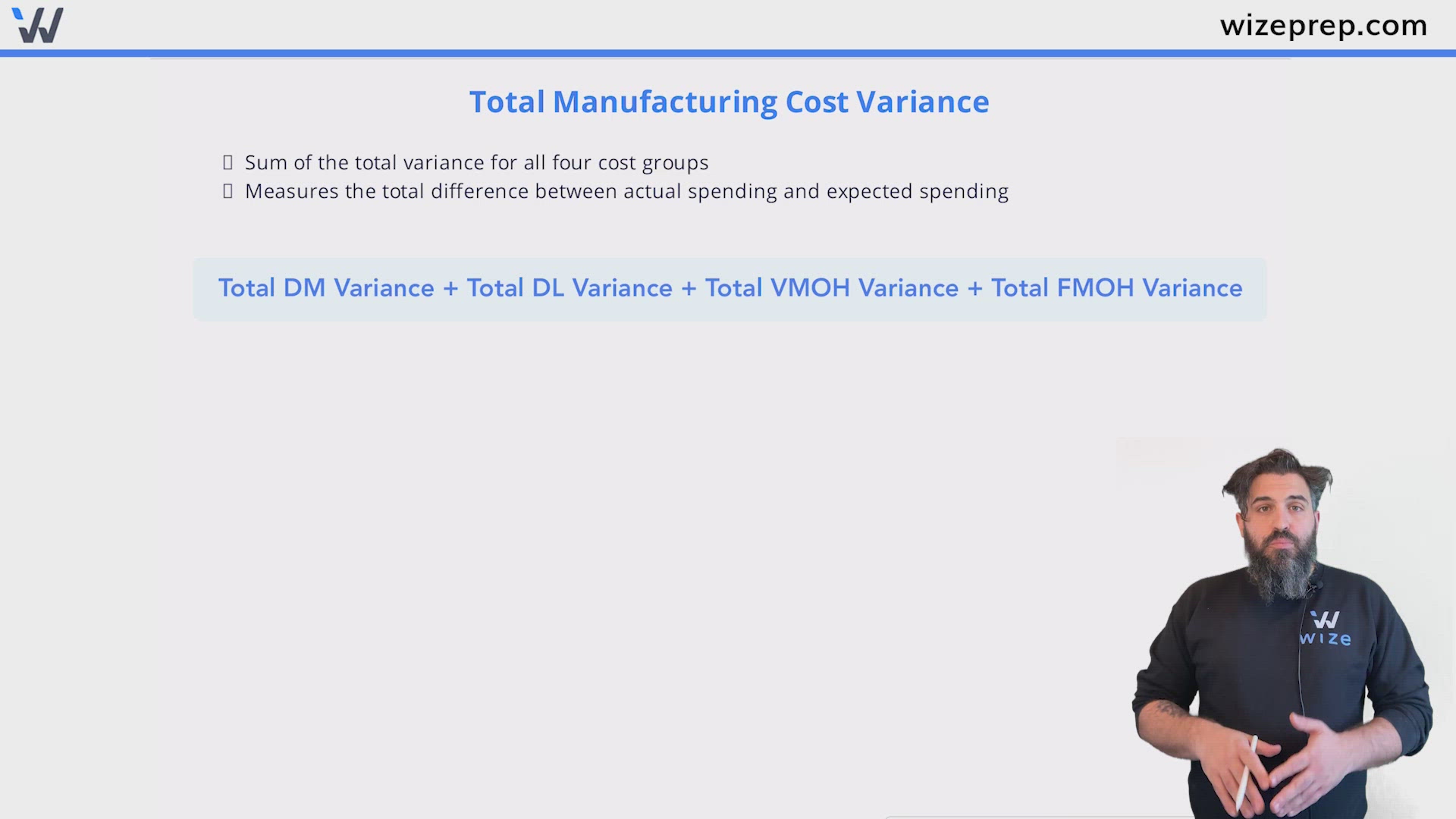

Total Manufacturing Cost Variance

- Sum of the total variance for all four cost groups

- Measures the total difference between actual spending and expected spending

0:00 / 0:00

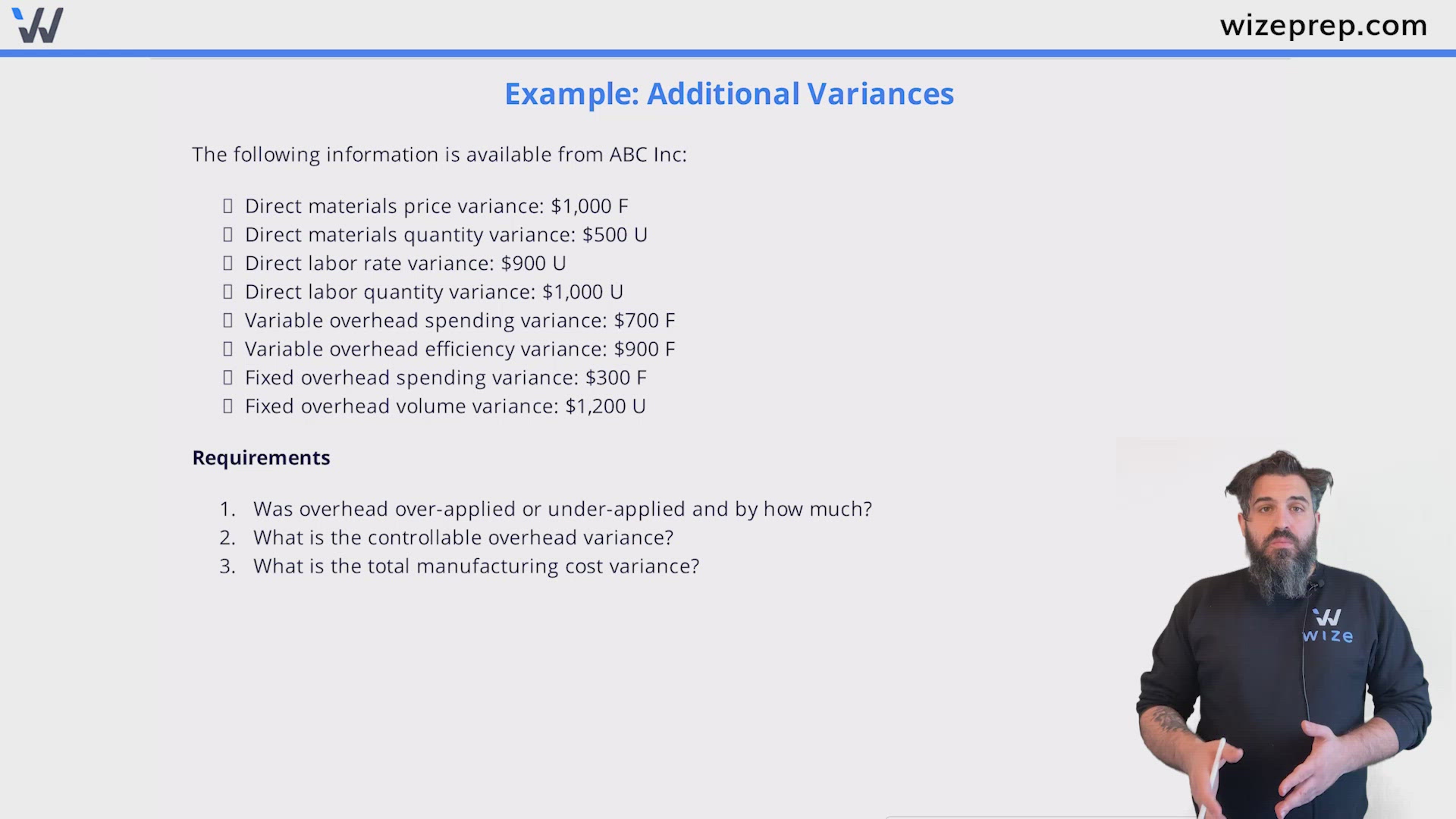

Example: Additional Variances

The following information is available from ABC Inc:

- Direct materials price variance: $1,000 F

- Direct materials quantity variance: $500 U

- Direct labor rate variance: $900 U

- Direct labor quantity variance: $1,000 U

- Variable overhead spending variance: $700 F

- Variable overhead efficiency variance: $900 F

- Fixed overhead spending variance: $300 F

- Fixed overhead volume variance: $1,200 U

Requirements

- Was overhead over-applied or under-applied and by how much?

- What is the controllable overhead variance?

- What is the total manufacturing cost variance?

Practice: Additional Variances

Romeo Inc. reported the following information in its variance report, some information is missing:

- Total direct material budget variance: $1,500 F

- Total direct labor budget variance: $1,200 F

- Variable overhead spending variance: $500 U

- Variable overhead efficiency variance: $1,000 F

- Fixed overhead spending variance: ?

- Fixed overhead volume variance: ?

- Controllable overhead variance: $800 F

- Overhead is under-applied by $200

Answer the following questions, do not use any symbols ($, %, !);

Use the first blank for the value and in the second blank enter F for favorable and U for unfavorable.

The fixed overhead spending variance is

The fixed overhead volume variance is

The total manufacturing cost variance is