Wize University Managerial Accounting Textbook > Process Costing

FIFO Unit Cost & Cost Reconciliation

Popular Courses

COMM 305

Concordia University

Managerial Accounting

University Study Guides

Managerial Accounting

University Study Guides

COMM 112

Queen's University

RSM222H1

University of Toronto

COMMERCE 2AB3

McMaster University

ACTG 2020

York University

COMM 1102

Dalhousie University

ACC 312

The University of Texas at Austin

ACIS 2116

Virginia Tech

ACG 2071

University of Central Florida

BUS1 21

San José State University

BUS-A 306

Indiana University - Bloomington

ACCT 2102

Temple University

ACCTG-202

San Diego State University

MGMT 20100

Purdue University

ACCTMIS 2300

Ohio State University

ACG 2071

University of Florida

ACCT 210

University of Arizona

BCOR 2303

University of Colorado Boulder

Unit Cost and Cost Reconciliation

Unit Costs

This section of the production cost report estimates an average cost per unit for each cost component (Direct Materials, Conversion Costs and Transferred-in Costs).

Cost Reconciliation

In this last section of the production cost report, we use the equivalent units and the unit costs to determine the total costs that will be transferred out of the work in process account and the account's ending balance.

0:00 / 0:00

Example: Unit Cost and Cost Reconciliation

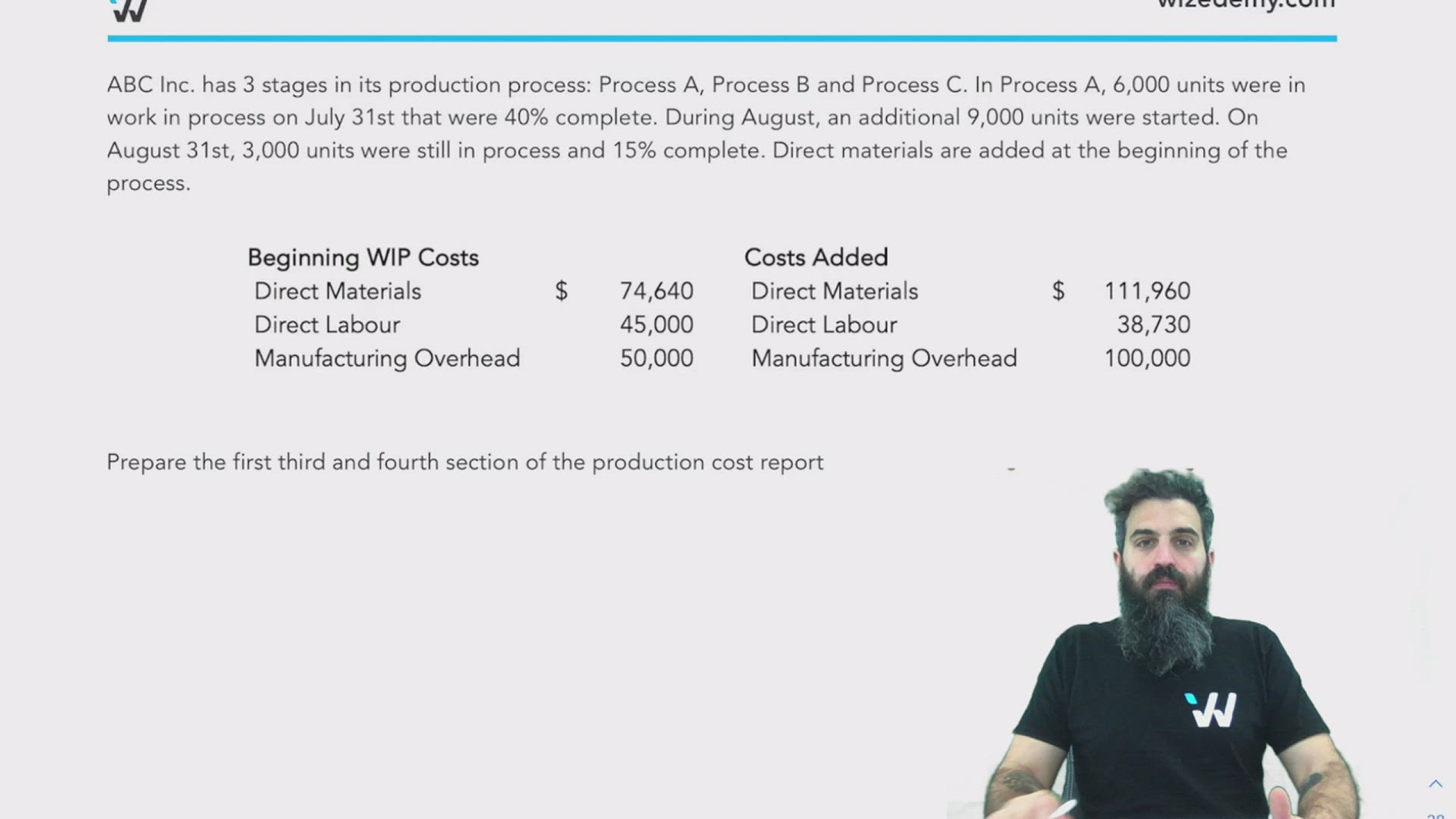

ABC Inc. has 3 stages in its production process: Process A, Process B and Process C. In Process A, 6,000 units were in work in process on July 31st that were 40% complete. During August, an additional 9,000 units were started. On August 31st, 3,000 units were still in process and 15% complete. Direct materials are added at the beginning of the process.

Prepare the first third and fourth section of the production cost report

Mark Yourself Question

- Grab a piece of paper and try this problem yourself.

- When you're done, check the "I have answered this question" box below.

- View the solution and report whether you got it right or wrong.

Practice: FIFO Method

Wize Company uses a process cost system. The Finishing Department adds materials at the beginning of the process and conversion costs are incurred uniformly throughout the process. Work in process on August 1 was 10,000 units that were 60% complete and Work in Process on August 31 was 9,000 units that were 25% complete. 35,000 units were transferred into the Finishing Department in August. Use the FIFO method.

Beginning WIP Costs

Direct Materials: $90,000

Direct Labour: $55,500

Manufacturing Overhead: $94,520

Transferred in costs: $179,300

Costs Added in August

Direct Materials: $174,600

Direct Labour: $92,700

Manufacturing Overhead: $100,000

Transferred in costs: $700,000

Prepare the production cost report