Wize University Introduction to Finance Textbook > Bond Valuation

Interest Rate Risk

Popular Courses

COMM 308

Concordia University

Intro to Finance

University Study Guides

Intro to Finance

University Study Guides

FINA 230

Concordia University

MGCR 341

McGill University

FIN 301

University of Alberta

FIN 300

Toronto Metropolitan University

COMM 121

Queen's University

FIN 2000

University of Guelph

FINC 341

Texas A&M University

COMMERCE 2FA3

McMaster University

COMM 2202

Dalhousie University

BU283

Wilfrid Laurier University

FIN 300

Arizona State University - Tempe

BUSFIN 3220

Ohio State University

FINE 2000

York University

FIN 301

Pennsylvania State University

BUS-F 255

Indiana University - Bloomington

FIN 3403

University of Central Florida

FIN 3403

University of Florida

0:00 / 0:00

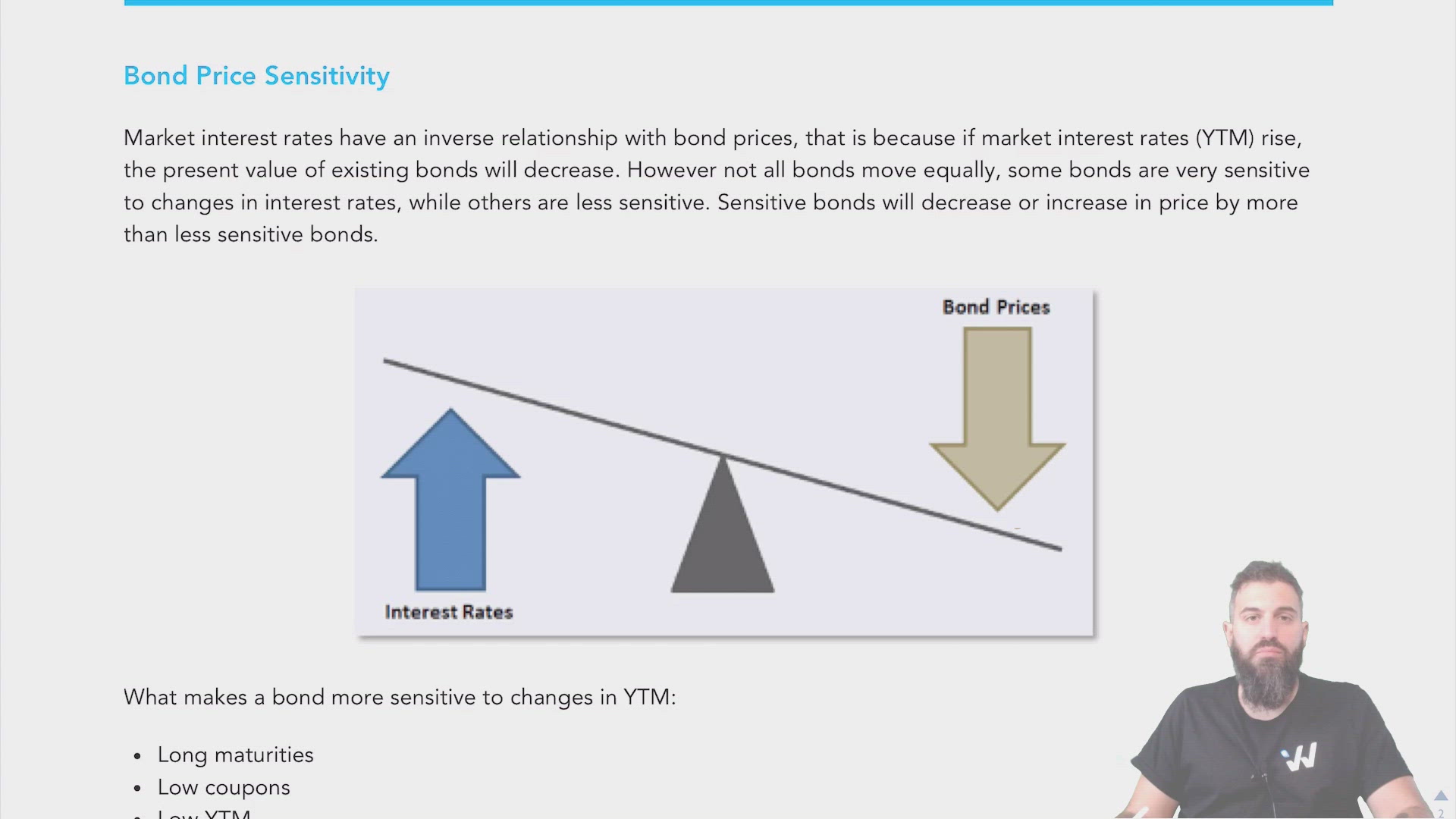

Bond Price Sensitivity

Market interest rates have an inverse relationship with bond prices, that is because if market interest rates (YTM) rise, the present value of existing bonds will decrease. However not all bonds move equally, some bonds are very sensitive to changes in interest rates, while others are less sensitive. Sensitive bonds will decrease or increase in price by more than less sensitive bonds.

What does the Price-Yield Curve tell us?

- Bonds are more sensitive to change in interest rates when yields are lower.

- Bonds are more sensitive when rates/yields decrease then when they increase.

Characteristics that increase bond sensitivity

- Long maturities

- Low coupons

- Low YTM

- Higher frequency of payments

For Example:

Consider the following two bonds, both have a face value of $1,000

Bond A: 10-year maturity, 5% coupons paid annually

Bond B: 30-year maturity, 5% coupons paid annually

Bond A: When YTM = 6%, Bond A is priced at $926.40; if YTM increases to 7% the price decreases by 7.21% to $859.53

Bond B: When YTM = 6%, Bond B is priced at $862.35; if YTM increases to 7% the price decreases by 12.82% to $751.82

Example: Bond Price Sensitivity

ABC Inc. has bonds outstanding with a $1,000 face value. The coupon rate on these bonds is 7% and coupons are paid annually. The bonds mature in 10 years. What is the percentage change in the price of the bond if the yield to maturity increases from 7% to 8%?

Practice: Bond Price Sensitivity

ABC Inc. has bonds outstanding with a $1,000 face value. The coupon rate on these bonds is 6% and coupons are paid semi-annually. The bonds mature in 8 years. The bond's are currently priced at par. What will be the percentage change in the price of the bond if the yield to maturity decreases by 50 basis points?

The percentage change in price is %

Round your final answer to 2 decimal places.