Popular Courses

COMM 217

Concordia University

ACCT 2301

The University of Texas at Dallas

Intro to Financial Accounting

General Course

COMM 293

University of British Columbia

Intro to Financial Accounting

University Study Guides

MGCR 211

McGill University

ACCT 1220

University of Guelph

Intro to Financial Accounting

University Study Guides

ACCT 217

University of Calgary

ADMS 2500

York University

ACCTG 211

University of Alberta

COMMERCE 1AA3

McMaster University

ACC 100

Toronto Metropolitan University

COMM 111

Queen's University

ADM 1340

University of Ottawa

BU127

Wilfrid Laurier University

RSM219H1

University of Toronto

COMM 1101

Dalhousie University

ACCT 2301

Houston

ACCT 2301

Houston

0:00 / 0:00

Assets

What is an Asset?

- Resource owned or controlled by a business

- Has an economic value

- Expected to provide a future economic benefit

0:00 / 0:00

Types of Assets

There are many types of asset, some as small as pencils and others are large as skyscrapers. Most assets can be classified into one of the following 5 categories.

Cash and Cash Equivalents

- This refers to the company's cash and all other assets that can be converted to cash immediately. Example:

- bank accounts

- foreign currency

- short-term investments maturity within 90 days

Receivables

A receivable is money owed to the company that is expected to be received in cash. The word 'receivable' is always preceded by a descriptor that tells us the reason for the receivable.

- Accounts Receivable (Trade Receivable): Money owed from customers for goods and services provided on account (on credit). Does not carry any interest.

- Notes Receivable: Money owed to the company as a result of a loan or other contractual agreement. Carries interest.

- Rent Receivable: Money owed to the company from a tenant for use of rented space.

- Interest Receivable: Money owed to the company from a borrower for interest related to a loan or note agreement.

Inventories

This refers to any assets kept in inventory by the company.

- Merchandise inventory: This refers to the goods on hand by the company that are available to be sold to customers as part of the company's primary business.

- Supplies inventory: This refers to inventory used as part of the company's operations. Examples:

- cleaning suppliers

- stationary

- spare parts.

Prepaid Expenses

- This refers to a payment for a bill or expense made before it has been used or incurred.

- Recorded as an asset until it the goods are received or services are used; once the goods or services have been received the cost is converted to an expense.

Property, Plant and Equipment

This refers to any long-term fixed assets controlled by the company. Given the long-term nature of these assets, companies also carry a contra-asset called accumulated depreciation, this account represents the amount of the asset's value that has been used by the company.

Examples:

- Buildings

- Equipment

- Machinery

- Land

- Furniture

0:00 / 0:00

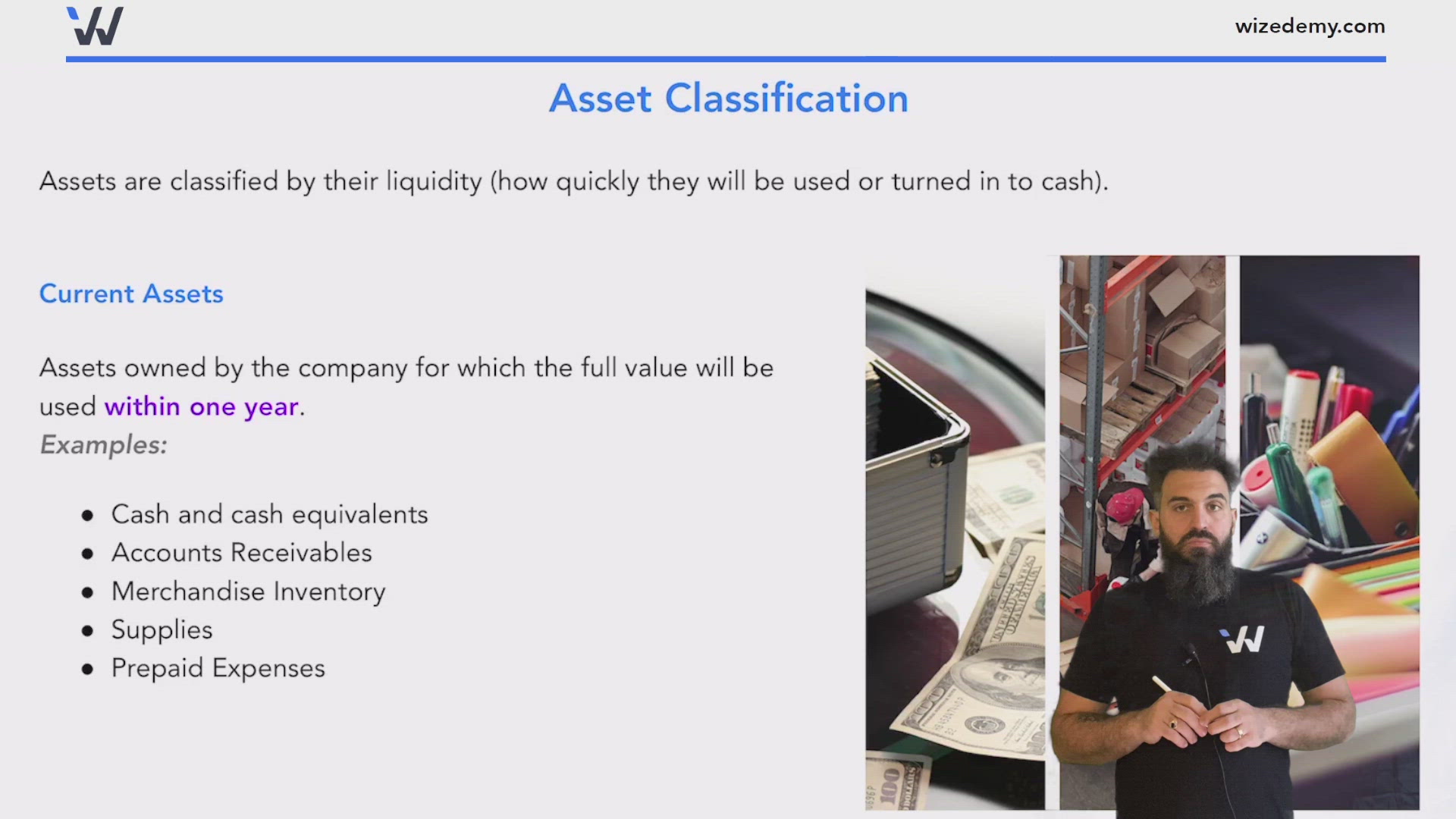

Asset Classification

Assets are classified by their liquidity (how quickly they will be used or turned in to cash).

Current Assets

Assets owned by the company for which the full value will be used within one year.

Examples:

- Cash and cash equivalents

- Accounts Receivables

- Merchandise Inventory

- Supplies

- Prepaid Expenses

Non-Current Assets

Assets owned by the company for which the full value will not be used in more than one year.

Examples:

- Buildings

- Equipment

- Furniture

- Machinery

- Land

- Long-Term Investments

- Patents and Trademarks

- Long-Term Receivables

0:00 / 0:00

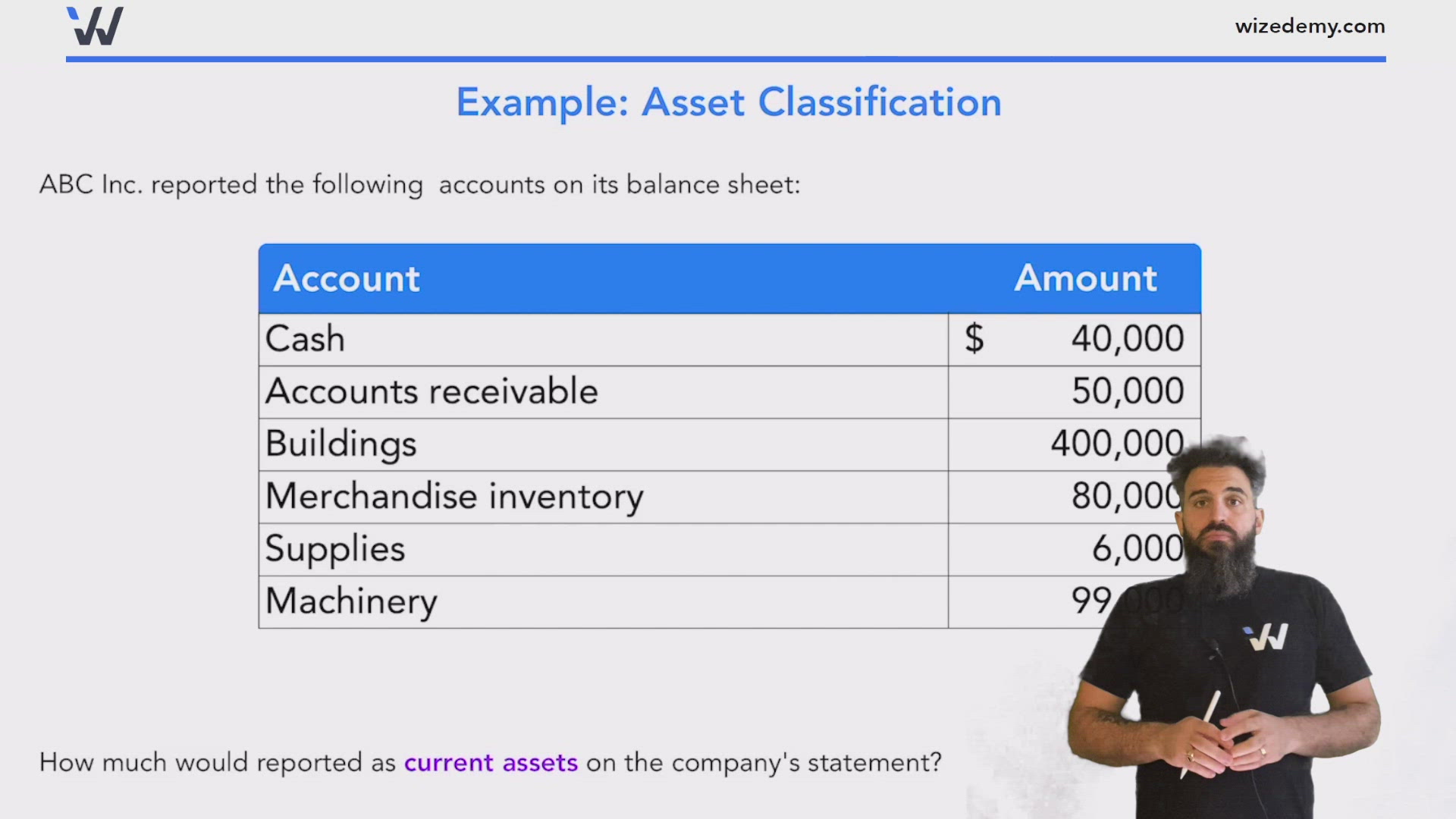

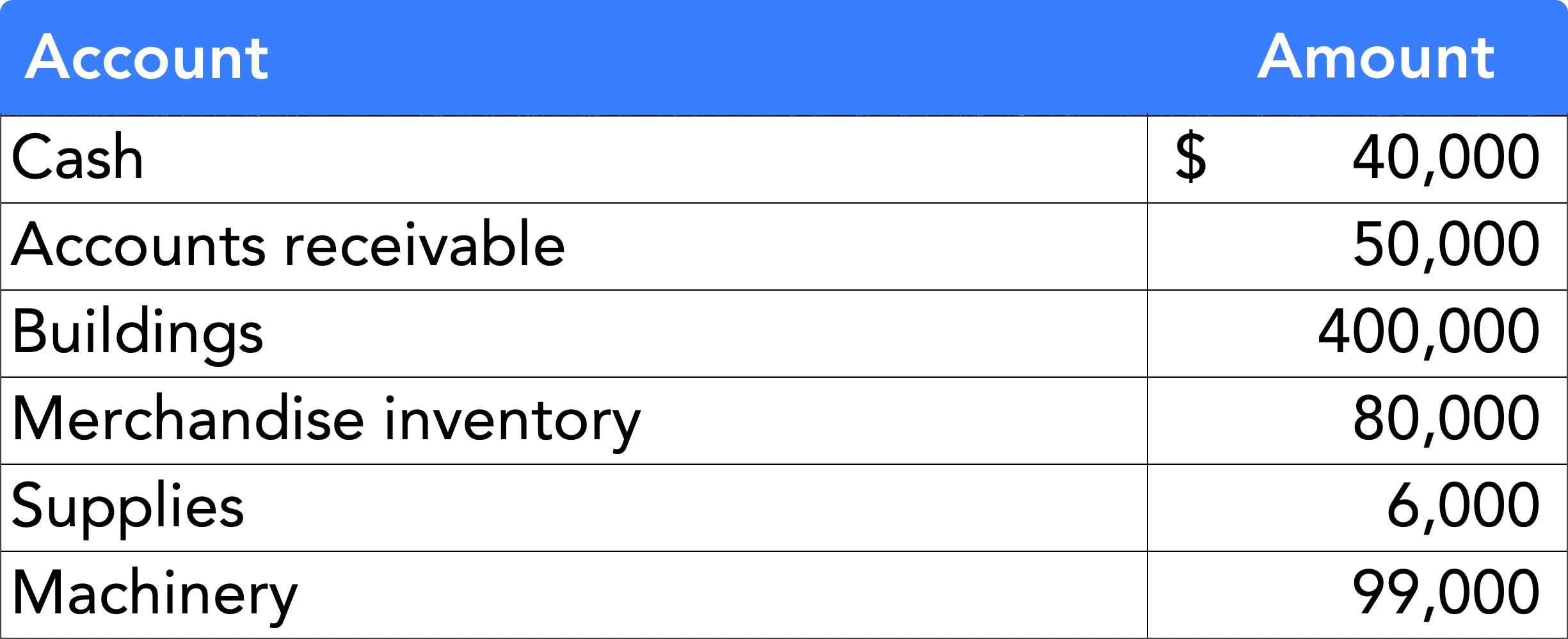

Example: Asset Classification

ABC Inc. reported the following accounts on its balance sheet:

How much would reported as current assets on the company's statement?

How much would be reported as non-current assets on the company's statement?

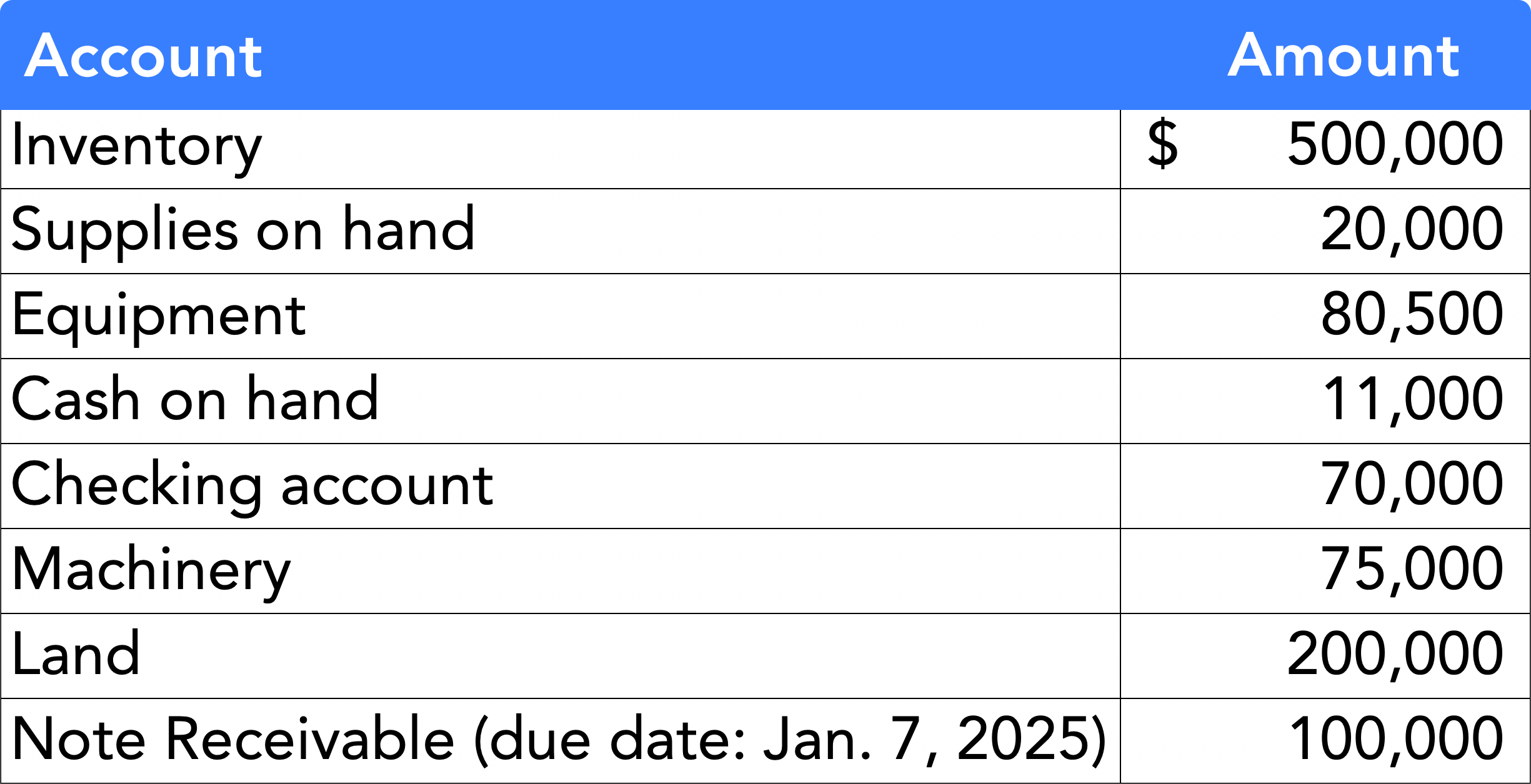

Practice: Asset Classification

On December 31, 2019 SOS Inc. reported the following accounts balances:

What is the total amount of current and non-current assets reported on the statement of financial position on this date?