Wize University Introduction to Financial Accounting Textbook > Long-Term Assets

Depreciation and Amortization

Popular Courses

COMM 217

Concordia University

ACCT 2301

The University of Texas at Dallas

Intro to Financial Accounting

General Course

COMM 293

University of British Columbia

Intro to Financial Accounting

University Study Guides

MGCR 211

McGill University

ACCT 1220

University of Guelph

Intro to Financial Accounting

University Study Guides

ACCT 217

University of Calgary

ADMS 2500

York University

COMMERCE 1AA3

McMaster University

ACCTG 211

University of Alberta

ACC 100

Toronto Metropolitan University

COMM 111

Queen's University

ADM 1340

University of Ottawa

BU127

Wilfrid Laurier University

RSM219H1

University of Toronto

ACCT 2301

Houston

ACCT 2301

Houston

COMM 1101

Dalhousie University

0:00 / 0:00

Depreciation and Amortization

Depreciation and amortization is necessary for a company to respect the matching principle. Since long-term assets are used for longer than a year, the costs incurred need to be spread out over time.

Depreciation and Amortization Expense

- Represents the portion of the assets cost that was used in the current period.

- Depreciation expense is used for tangible assets (property, plant and equipment)

- Amortization expense is used for intangible assets

Factors that Affect Depreciation

- Useful life: How long the company estimates it will use the asset for.

- For intangible assets, cost is amortized over the shorter of the useful life or the legal life.

- Residual value: The value the company estimates will remain at the end of the asset's life, also called salvage value.

- Depreciation method: The type of depreciation used, typically depends on the type of asset.

- Straight-line method

- Declining-balance method

- Units of production method

Accumulated Depreciation

- Contra-asset

- Represents the total amount of depreciation on an asset since it was acquired.

- Decreases the carrying value of an asset.

Journalizing Depreciation

- Adjusting journal entry

- Debit depreciation expense

- Credit accumulated depreciation of specific asset

0:00 / 0:00

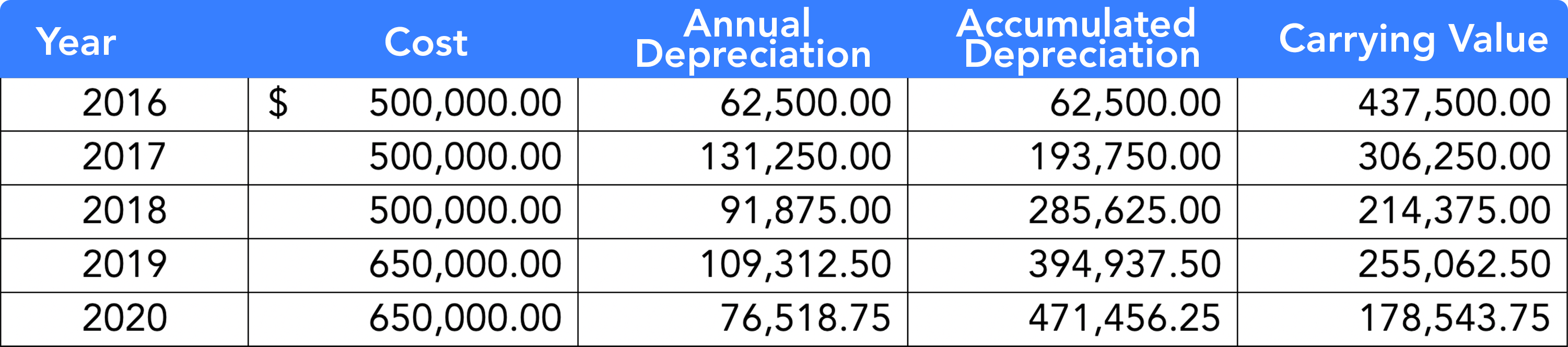

Amortization Table

The amortization table is a useful tool for organizing and keeping track of the depreciation or amortization of a company's assets.

For each year the asset has been owned, it shows the:

- Cost

- Any additional capital expenditures are added to cost in the year they occur

- Annual depreciation

- Accumulated depreciation

- Carrying Value

- Cost - Accumulated depreciation