Popular Courses

COMM 305

Concordia University

Managerial Accounting

University Study Guides

Managerial Accounting

University Study Guides

COMM 112

Queen's University

ACC 406

Toronto Metropolitan University

ACCTG 322

University of Alberta

ACCT 2230

University of Guelph

ADM 2341

University of Ottawa

RSM222H1

University of Toronto

COMMERCE 2AB3

McMaster University

ACTG 2020

York University

COMM 1102

Dalhousie University

ACC 312

The University of Texas at Austin

ACC 242

Arizona State University - Tempe

ACC 202

Michigan State University

ACIS 2116

Virginia Tech

ACG 2071

University of Central Florida

BUS1 21

San José State University

BUS-A 306

Indiana University - Bloomington

ACCT 2102

Temple University

0:00 / 0:00

Manufacturing Costs

Manufacturing costs are the costs related to the purchasing of raw materials, and to the activities that convert the raw materials into finished goods.

All manufacturing costs are classified as:

- Direct materials

- Direct labor

- Manufacturing overhead

0:00 / 0:00

Direct Material

Raw Materials

- All material used in production

- Purchased from suppliers

- Kept in inventory until used

- When raw materials are used, they are classified as direct or indirect materials

Direct Materials

- Materials that end up in the final product and can be directly associated to the product.

- Significant elements of the final product

Indirect Materials

- Materials that do not end up in the final product

- Materials that end up in the final product but cannot be direct or accurately traced to that product.

- Not a significant element of the final product

- Accounted for as part of manufacturing overhead

Examples of direct and indirect materials in the production of cars

0:00 / 0:00

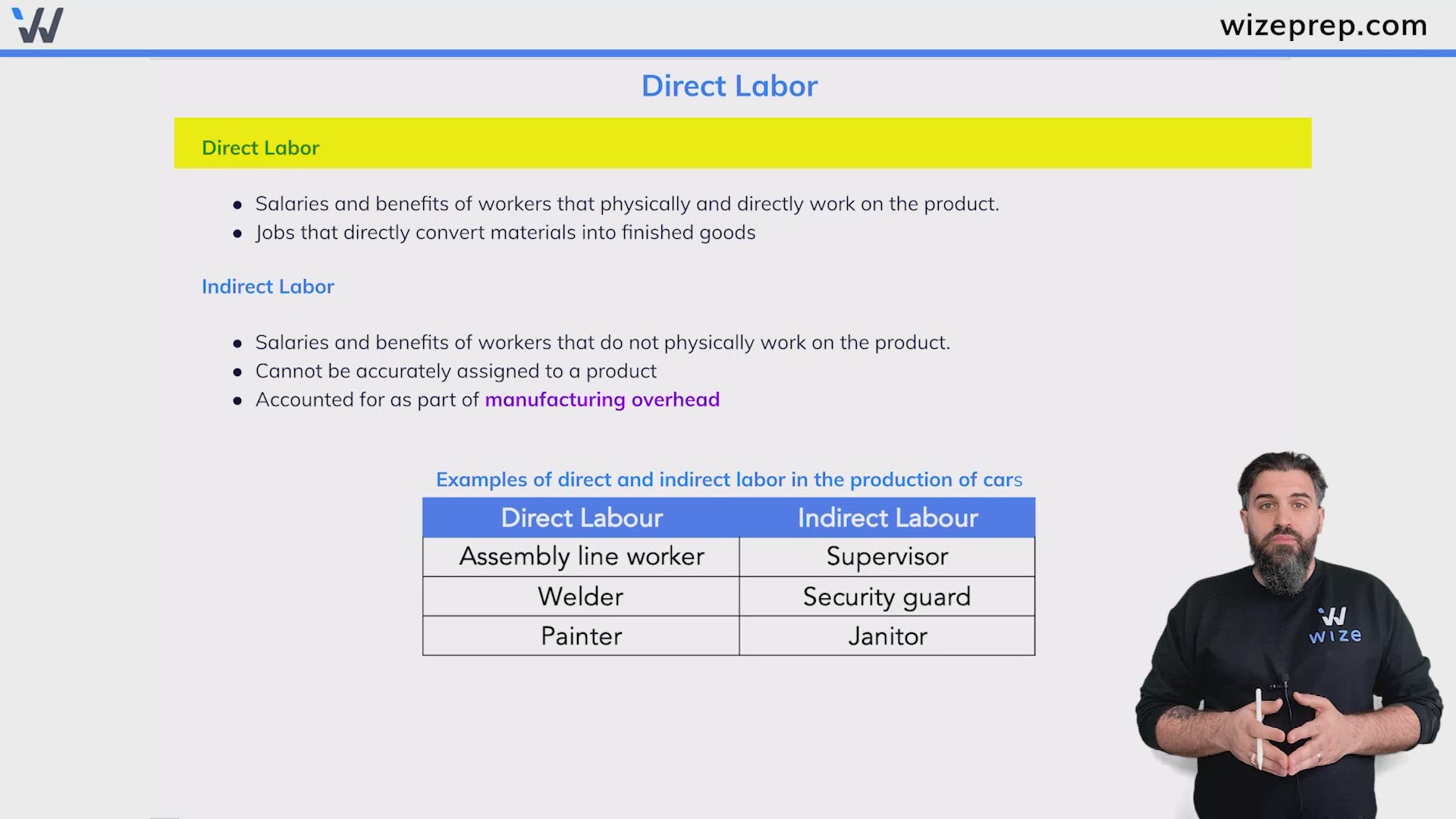

Direct Labor

Direct Labor

- Salaries and benefits of workers that physically and directly work on the product.

- Jobs that directly convert materials into finished goods

Indirect Labor

- Salaries and benefits of workers that do not physically work on the product.

- Cannot be accurately assigned to a product

- Accounted for as part of manufacturing overhead

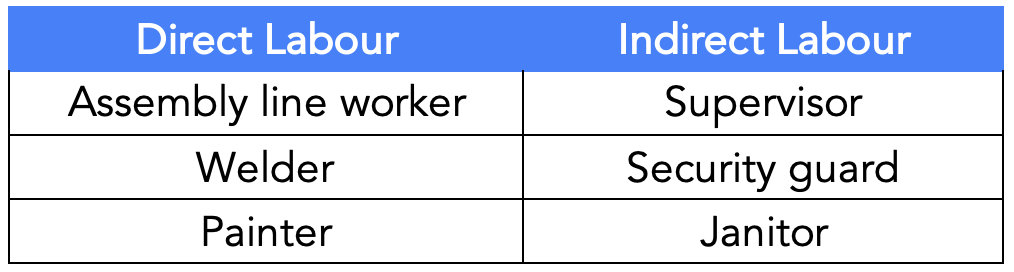

Examples of direct and indirect labor in the production of cars

0:00 / 0:00

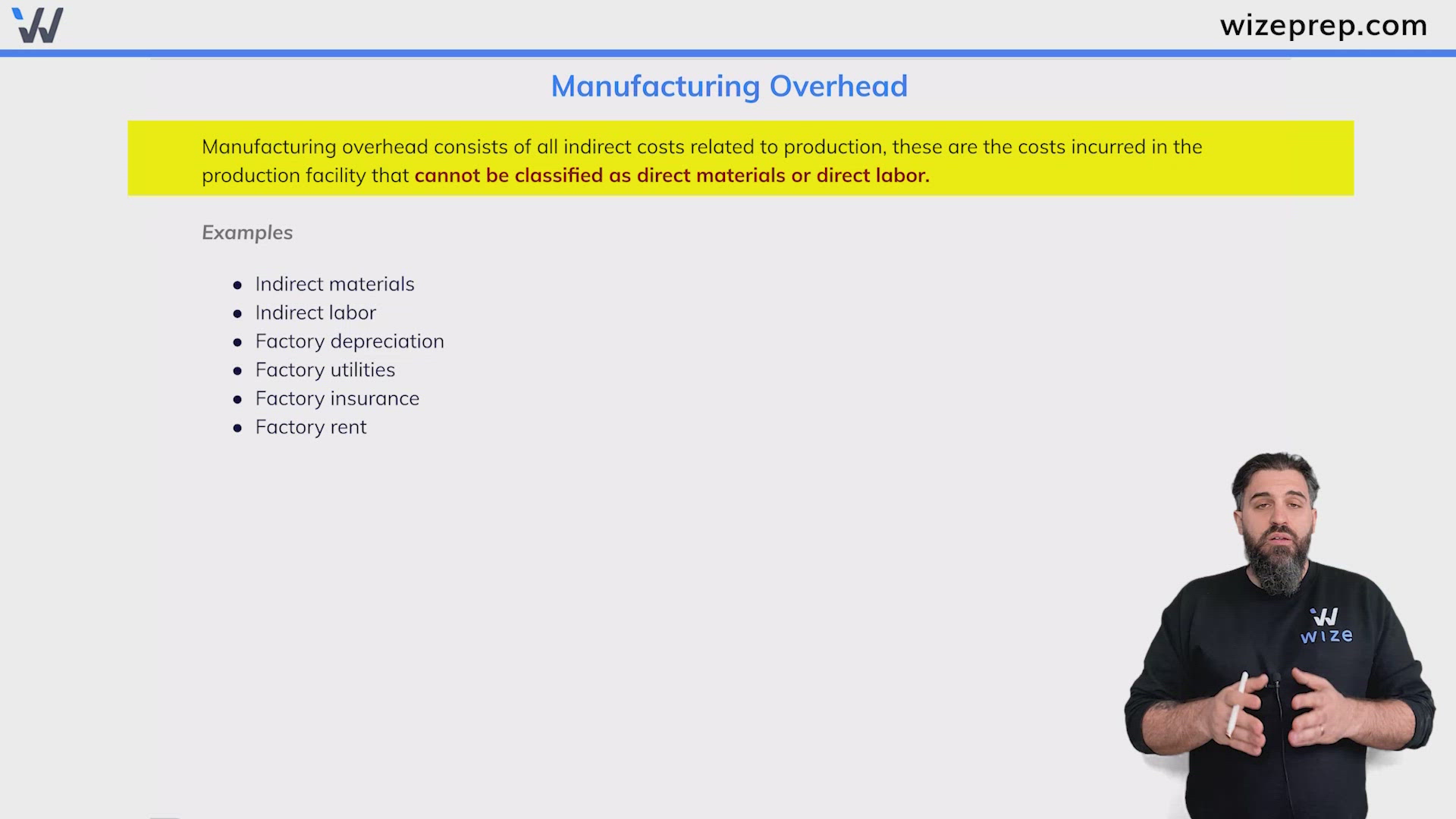

Manufacturing Overhead

Manufacturing overhead consists of all indirect costs related to production, these are the costs incurred in the production facility that cannot be classified as direct materials or direct labor.

Examples

- Indirect materials

- Indirect labor

- Factory depreciation

- Factory utilities

- Factory insurance

- Factory rent

Practice: Manufacturing Costs

Select the best answer(s) for the following questions

Which of the following is most likely to be considered a direct material in the production of a wooden table?