Wize University Introduction to Finance Textbook > Options

Put-Call Parity

Popular Courses

Intro to Finance

University Study Guides

Intro to Finance

University Study Guides

FIN 301

University of Alberta

FINC 341

Texas A&M University

COMM 2202

Dalhousie University

BU283

Wilfrid Laurier University

FIN 300

Arizona State University - Tempe

BUSFIN 3220

Ohio State University

FIN 301

Pennsylvania State University

BUS-F 255

Indiana University - Bloomington

FIN 3403

University of Central Florida

FIN 3403

University of Florida

FIN 320

California State University - Fullerton

FINC-UB 7

New York University

FINC-UB 2

New York University

BMGT340

University of Maryland - College Park

BUS1 170

San José State University

BUSM 2021

University of Colorado Boulder

33:390:203

Rutgers University - New Brunswick (Busch)

0:00 / 0:00

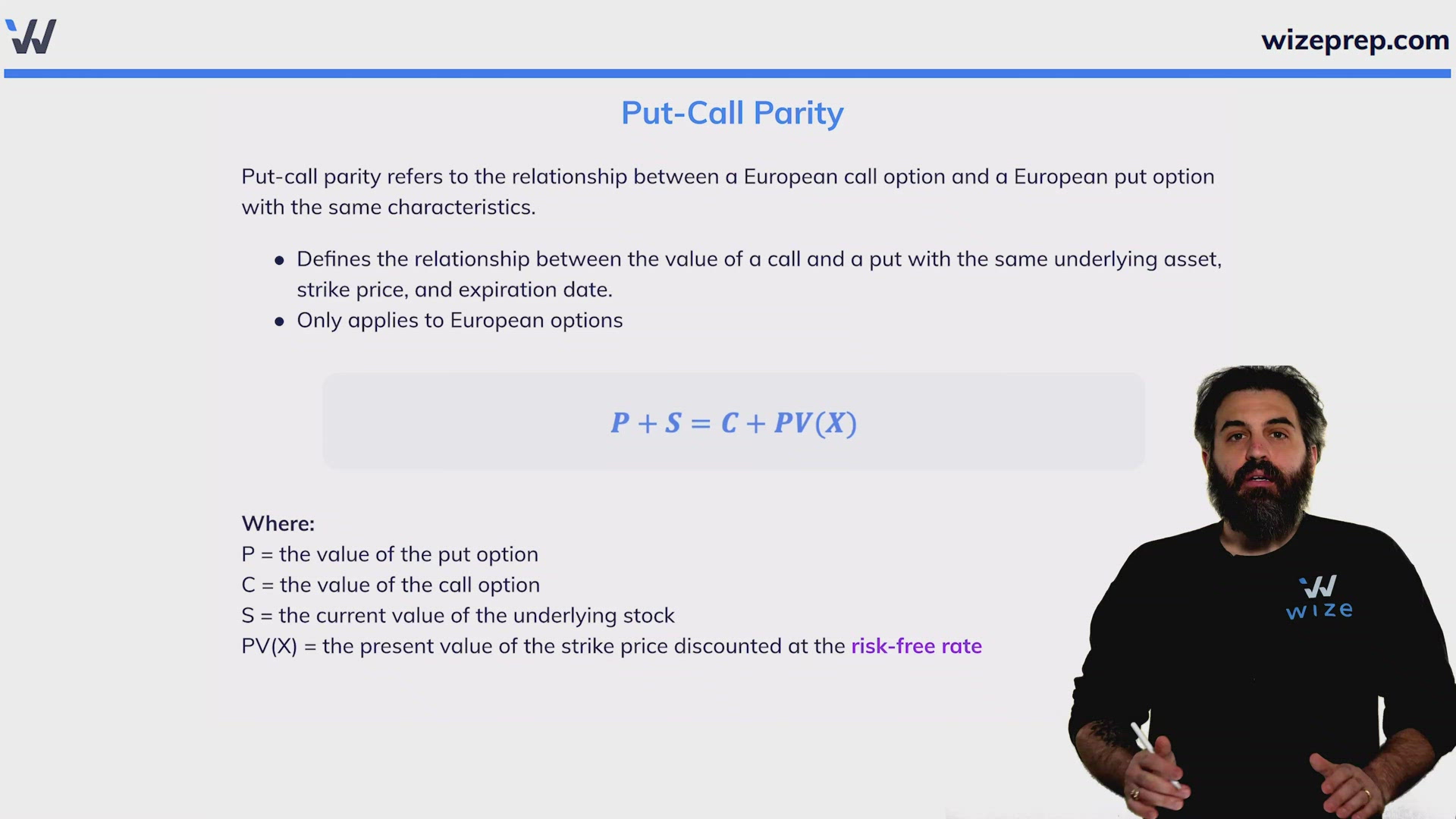

Put-Call Parity

Put-call parity refers to the relationship between a European call option and a European put option with the same characteristics.

- Defines the relationship between the value of a call and a put with the same underlying asset, strike price, and expiration date.

- Only applies to European options

Where:

P = the value of the put option

C = the value of the call option

S = the current value of the underlying stock

PV(X) = the present value of the strike price discounted at the risk-free rate

0:00 / 0:00

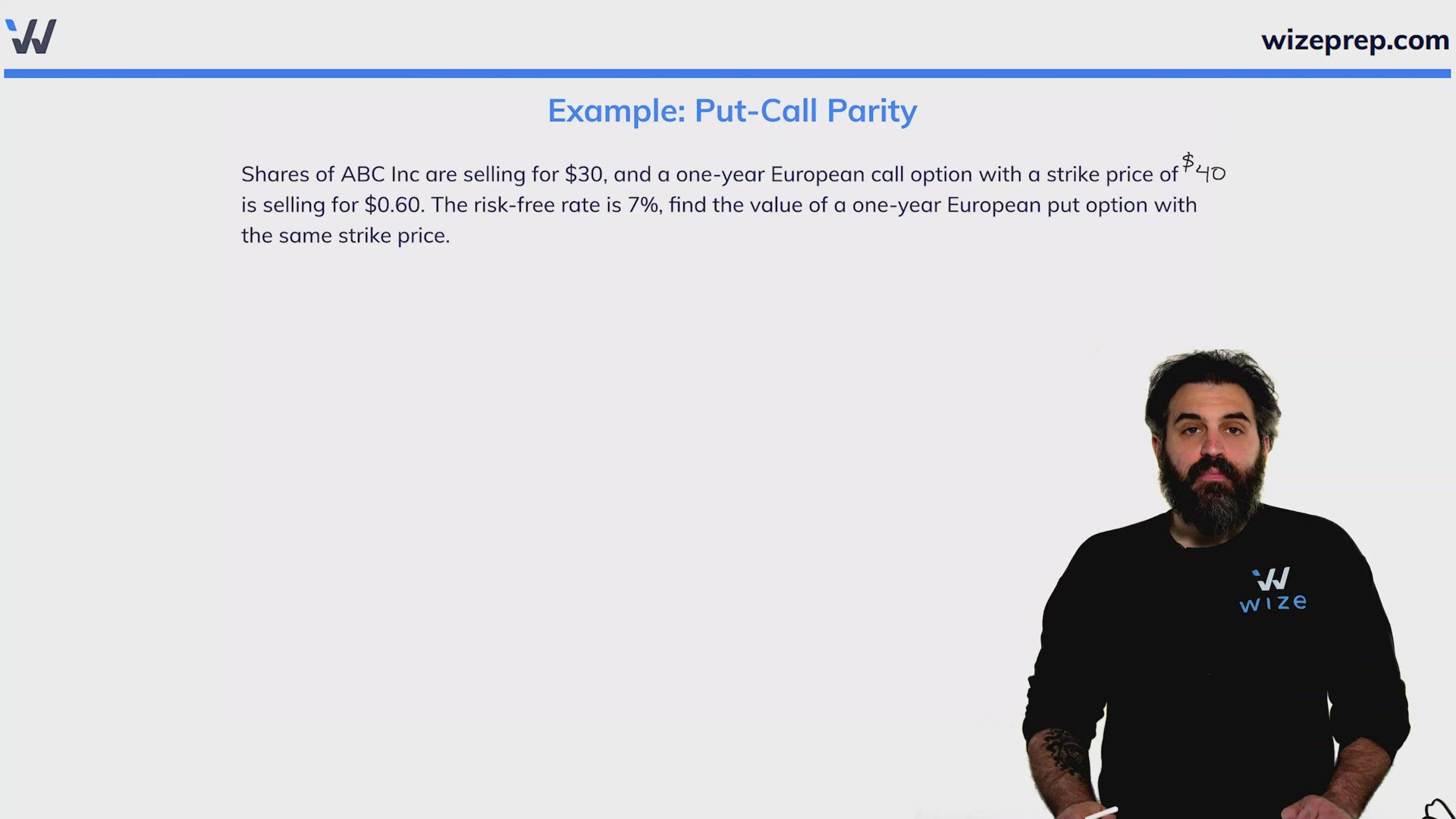

Example: Put-Call Parity

Shares of ABC Inc are selling for $30, and a one-year European call option with a strike price of $40 is selling for $0.60. The risk-free rate is 7%, find the value of a one-year European put option with the same strike price.

Practice: Put-Call Parity

Shares of XYZ Corporation are trading for $75 and a six-month European put option on those shares with a strike price of $60 is selling for $1.20. If the risk-free rate is 6%, find the value of a six-month European call option with the same strike price.

Round your final answer to 2 decimal places

| Value of the call option | $ |